COVID-19: Additional Actions Needed to Improve Accountability and Program Effectiveness of Federal Response

Fast Facts

As the nation continues to respond to and recover from the COVID-19 pandemic, recent increases in cases have hampered these efforts and created new challenges.

In our 8th comprehensive report, we found more ways to help the federal government address the pandemic and prepare for future emergencies. Specifically, we made 16 new recommendations, including on ways to ensure proper use of relief funds, oversee worker safety and health, and reduce fraud risks.

To date, federal agencies have fully addressed 33 of our 209 recommendations on the COVID-19 response since June 2020, and partially addressed another 48.

Highlights

What GAO Found

As the nation continues to respond to, and recover from, the COVID-19 pandemic, increases in COVID-19 cases in July, August, and September 2021, primarily due to the Delta variant of the virus, have hampered these efforts. From the end of July 2021 to September 23, 2021, the number of new cases reported each day generally exceeded 100,000, according to Centers for Disease Control and Prevention (CDC) data. This was a daily case count not seen since February 2021 (see figure).

Reported COVID-19 Cases per Day in the U.S., Mar. 1, 2020–Sept. 23, 2021

Meanwhile, COVID-19 vaccination efforts continue. As of September 23, 2021, about 64 percent of the U.S. population eligible for vaccination (those 12 years and older), or almost 183 million individuals, had been fully vaccinated, according to CDC.

The government must remain vigilant and agile to address the evolving COVID-19 pandemic and its cascading impacts. Furthermore, as the administration implements the provisions in the COVID-19 relief laws, the size and scope of these efforts—from distributing funding to implementing new programs—demand strong accountability and oversight. In that vein, GAO has made 209 recommendations across its body of COVID-19 reports issued since June 2020. As of September 30, 2021, agencies had addressed 33 of these recommendations, resulting in improvements including increased oversight of relief payments to individuals and improved transparency of decision-making for emergency use authorizations for vaccines and therapeutics. Agencies partially addressed another 48 recommendations. GAO also raised four matters for congressional consideration, three of which remain open.

In this report, GAO is making 16 new recommendations, including recommendations related to fiscal relief funds for health care providers, recovery funds for states and localities, worker safety and health, and assessing fraud risks to unemployment insurance programs. GAO’s recommendations, if swiftly and effectively implemented, can help improve the government’s ongoing response and recovery efforts as well as help it to prepare for future public health emergencies. GAO’s new findings and recommendations, where applicable, are discussed below.

Relief for Health Care Providers

A total of $178 billion has been appropriated to the Provider Relief Fund (PRF) to reimburse eligible providers for health care–related expenses or lost revenues attributable to COVID-19. As of August 31, 2021, the Department of Health and Human Services (HHS) had allocated and disbursed about $132.5 billion of this amount and had allocated but not yet disbursed about $21.5 billion; the remaining $24.1 billion was unallocated and undisbursed. On September 10, 2021, HHS announced that $17 billion of the previously unallocated $24.1 billion would be allocated for a general distribution to a broad range of providers who could document COVID-related revenue loss and expenses. HHS expected to begin disbursing the funds in December 2021.

As of September 2021, HHS’s Health Resources and Services Administration (HRSA) had not established time frames for implementing and completing post payment reviews for all PRF payments. In addition, the agency had not finalized procedures for recovery of overpayments or recovered the bulk of the overpayments that it had already identified.

Without post-payment oversight to help ensure that relief payments are made only to eligible providers in correct amounts and to identify unused payments or payments not properly used, HHS cannot fully address stated payment integrity risks for the PRF and seek to recover overpayments, unused payments, or payments not properly used. GAO recommends that HRSA take steps to finalize and implement post-payment oversight. Specifically, HRSA should establish time frames for completing post-payment reviews to promptly address identified risks and identify overpayments made from the PRF, such as payments made in incorrect amounts or payments to ineligible providers; and it should finalize procedures and implement post-payment recovery of any PRF overpayments, unused payments, or payments not properly used. HHS—which includes HRSA—partially agreed with these recommendations.

Coronavirus State and Local Fiscal Recovery Funds

In March 2021, the American Rescue Plan Act of 2021 (ARPA) appropriated $350 billion to the Department of the Treasury (Treasury) to provide payments from the Coronavirus State and Local Fiscal Recovery Funds (CSLFRF). The CSLFRF allocates funds to states, the District of Columbia, localities, tribal governments, and U.S. territories to cover a broad range of costs stemming from the COVID-19 pandemic’s fiscal effects. According to Treasury data, it had distributed approximately $240 billion from the CSLFRF to recipients as of August 31, 2021 (see figure).

Coronavirus State and Local Fiscal Recovery Funds Allocations and Treasury Distributions as of Aug. 31, 2021, by Recipient Type

As of July 2021, some of the 48 states that responded to GAO’s survey reported that they had somewhat less than or much less than sufficient capacity to report on their use of CSLFRF allocation consistent with federal requirements (17 of 48 states), capacity to disburse the funds (13 of 48 states), and apply appropriate internal controls and respond to inquiries about requirements (10 of 48 states). In addition, most states (44 of 48) reported that they had taken or planned to take additional steps—such as hiring new staff or reassigning existing staff—to help them manage their CSLFRF allocations.

As of August 2021, Treasury was developing—but had not finalized or documented—key internal processes and control activities to monitor recipients’ use of their CSLFRF allocations for allowable purposes and to respond to internal control and compliance findings. According to officials, these internal processes and control activities were in the development stage, partly because of the short time frame since ARPA’s enactment and because Treasury’s Office of Recovery Programs, established in April 2021, continues to work to recruit and onboard key team members.

Until Treasury properly designs and documents policies and procedures to guide CSLFRF program officials and other responsible oversight parties in the Office of Recovery Programs, there is a risk that key control activities needed to help ensure program management fulfills its recipient monitoring and oversight responsibilities may not be established or applied effectively and consistently. This risk may be particularly acute with respect to monitoring state and local recipients that face capacity challenges in managing their CSLFRF allocations in accordance with federal requirements, as some survey respondents noted. GAO recommends that Treasury design and document timely and sufficient policies and procedures for monitoring CSLFRF recipients to provide assurance that recipients are managing their allocations in compliance with laws, regulations, agency guidance, and award terms and conditions. Treasury agreed with the recommendation.

Unemployment Insurance Fraud Risk Management

GAO continues to have concerns about potential fraud in the unemployment insurance (UI) program, including concerns about Department of Labor (DOL) efforts to assess and manage program fraud risks. During the pandemic, fraudulent and potentially fraudulent activity has increased substantially and new types of fraud have emerged, according to DOL officials. For example, in June 2021, DOL’s Office of Inspector General reported that it had identified nearly $8 billion in potentially fraudulent UI benefits paid from March 2020 through October 2020. Improper payments have also been a long-standing concern in the regular unemployment insurance program, suggesting that the program may be vulnerable to fraud. While DOL continues to identify and implement strategies to address potential fraud and has some ongoing program integrity activities, it has not comprehensively assessed fraud risks in alignment with leading practices identified in GAO’s Fraud Risk Framework, which by law must be incorporated in guidelines established by the Office of Management and Budget for agencies.

DOL has not clearly assigned defined responsibilities to a dedicated entity for designing and overseeing fraud risk management activities. Without a dedicated entity with defined responsibilities to lead antifraud initiatives, including the process of assessing fraud risks to UI programs, DOL may not be strategically managing UI fraud risks. GAO recommends that DOL designate a dedicated entity and document its responsibilities for managing the process of assessing fraud risks to the unemployment insurance program, consistent with leading practices as provided in GAO’s Fraud Risk Framework. This entity should have, among other things, clearly defined and documented responsibilities and authority for managing fraud risk assessments and for facilitating communication among stakeholders regarding fraud-related issues. DOL neither agreed nor disagreed with this recommendation.

DOL also has not comprehensively assessed UI fraud risks in alignment with leading practices identified in GAO’s Fraud Risk Framework. These leading practices call for federal managers to plan regular fraud risk assessments and determine their fraud risk profile, among other things. Such assessments would provide reasonable assurance that DOL has identified the most significant fraud risks for the regular UI program that will exist after the pandemic. For example, some fraud risks identified in the CARES Act UI programs may continue to exist in the regular UI program after the temporary UI programs expire. GAO recommends that DOL (1) identify inherent fraud risks facing the unemployment insurance program, (2) assess the likelihood and impact of inherent fraud risks facing the program, (3) determine fraud risk tolerance for the program, (4) examine the suitability of existing fraud controls in the program and prioritize residual fraud risks, and (5) document the fraud risk profile for the program. DOL neither agreed nor disagreed with these recommendations.

FEMA’s Disaster Relief Fund and Assistance to State, Local, Tribal, and Territorial Governments

The Federal Emergency Management Agency (FEMA) has used the Disaster Relief Fund to respond to the COVID-19 pandemic—the first time the fund has been used during a nationwide public health emergency. For example, from September 1, 2020 to August 31, 2021, FEMA obligated a total of approximately $26.8 billion through one type of disaster assistance, Public Assistance, for emergency protective measures, such as eligible medical care, the purchase and distribution of food, and distribution of personal protective equipment.

GAO found that FEMA inconsistently interpreted and applied its policies for expenses eligible for COVID-19 Public Assistance within and across its 10 regions. For example, officials in one state said that FEMA at one point had deemed the provision of personal protective equipment at correctional facilities as ineligible for reimbursement in their region but that states in other regions had received reimbursement for the same expense. These inconsistencies were due to, among other things, changes in policies as FEMA used the Public Assistance program for the first time to respond to a nationwide emergency. FEMA officials stated that it was difficult to ensure consistency in policies as different states and regions are not experiencing the same things at the same time.

FEMA is likely to receive applications for reimbursement for a larger number of projects than it estimated earlier in 2021, given the surge in COVID-19 cases this summer. To improve the consistency of the agency’s interpretation and application of the COVID-19 Public Assistance policy, GAO recommends that FEMA further clarify and communicate eligibility requirements nationwide. GAO also recommends that FEMA require the agency’s Public Assistance employees in the regions and at its Consolidated Resource Centers to attend training on changes to COVID-19 Public Assistance policy. The Department of Homeland Security—which includes FEMA— agreed with both of these recommendations.

Loans for Aviation and Other Eligible Businesses

Treasury has executed 35 loan agreements with certain aviation businesses and other businesses deemed critical to maintaining national security. These loans have totaled about $22 billion of the $46 billion authorized by the CARES Act for loans and loan guarantees to such businesses. As directed by the CARES Act, Treasury required certain loan recipients to provide financial assets, such as warrants that give the federal government an option to buy shares of stock at a predetermined price before a specified date, to protect taxpayer interests.

According to Treasury officials, it is likely that, if the airline industry continues to recover and borrowers do not default, the warrants could have higher values than the predetermined price Treasury would have to pay to act on them. Treasury has not exercised any of the warrants for stock it received from nine businesses, nor has it developed policies and procedures for determining when to act on the warrants to benefit the taxpayer. GAO recommends that Treasury develop policies and procedures to determine when to act on warrants obtained as part of the loan program for aviation and other eligible businesses to benefit the taxpayers. Treasury agreed with this recommendation.

Payroll Support Assistance to Aviation Businesses

As of September 2021, Treasury had made payments totaling $59 billion of $63 billion provided for the Payroll Support Programs to support aviation business. These payments were to be used exclusively for the continuation of wages, salaries, and benefits.

Similar to Treasury’s requirement for loans for aviation and other eligible businesses, Treasury required certain Payroll Support Program recipients to provide warrants, as allowed by the CARES Act. As of September 2021, 14 recipients had provided a total of 58 million warrants.

As Treasury continues to hold these warrants for stock purchases, the warrants may increase in value as the airline industry recovers. Treasury has not exercised any of the warrants for stock it holds in the 14 businesses, nor has it documented policies and procedures to guide when to act on the warrants to fulfill the statutory purpose to provide appropriate compensation to the federal government. GAO recommends that Treasury develop policies and procedures to determine when to act on warrants obtained as part of the Payroll Support Program to provide appropriate compensation to the federal government. Treasury agreed with this recommendation.

COVID-19 Testing

Use is increasing for antigen tests, one of two types of COVID-19 diagnostic and screening tests for which HHS’s Food and Drug Administration has issued emergency use authorizations. These “rapid” antigen tests typically have a turnaround time of about 30 minutes or less for results, compared with 1 to 3 days for molecular tests, the second type of test HHS authorized. Antigen tests can be conducted at doctors’ offices or in homes or other settings; some antigen tests can be conducted without a prescription.

Since June 2020, HHS has worked to encourage and improve the reporting of antigen testing data to local, state, and federal health officials. However, HHS officials told GAO reporting of antigen test results is incomplete, which prevents HHS from using antigen testing data for COVID-19 surveillance. HHS is taking additional steps aimed at improving reporting of antigen test data. For example, officials told GAO that HHS will continue to make enhancements to data reporting by building reporting methods into the testing process, such as for testing in schools and workplaces.

HHS is also considering surveillance approaches to supplement or enhance current surveillance efforts. For example, HHS is exploring wastewater surveillance approaches, which provide data that can complement and confirm other forms of surveillance for COVID-19 and an efficient pooled community sample that is particularly useful in areas where timely COVID-19 clinical testing is underutilized or unavailable, according to HHS officials.

Worker Safety and Health

The Occupational Safety and Health Administration (OSHA) faced challenges in enforcing workplace safety and health standards during the COVID-19 pandemic, but the agency has not assessed lessons learned or promising practices. According to inspectors from area offices, they faced challenges related to resources and to communication and guidance, such as a lack of timely guidance from OSHA headquarters. GAO recommends that OSHA assess—as soon as feasible and, as appropriate, periodically thereafter—various challenges related to resources and to communication and guidance that the agency has faced in its response to the COVID-19 pandemic and take related actions as warranted. The Department of Labor—which includes OSHA—partially agreed with this recommendation.

Advance Child Tax Credit Payments

ARPA temporarily expanded eligibility for the child tax credit (CTC) to additional qualified individuals by eliminating a requirement that individuals must earn a minimum amount annually to be eligible. ARPA also temporarily increased the maximum amount of the CTC from $2,000 per qualifying child to $3,000 or $3,600, depending on the child’s age. As required by ARPA, the Internal Revenue Service (IRS) and Treasury are responsible for issuing half of the CTC through periodic advance payments, known as advance CTC payments.

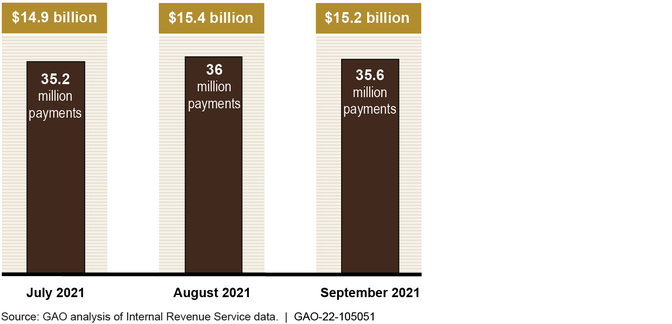

IRS reported disbursing more than 106 million advance payments totaling over $45.5 billion as of September 25, 2021 (see figure).

Dollar Amount and Count of Advance Child Tax Credit Payments, by Month, as of Sept. 25, 2021

IRS is conducting and planning several outreach efforts to increase the public’s awareness of advance CTC payments. However, IRS and Treasury have not developed a comprehensive estimate of individuals who are potentially eligible for advance CTC payments and the agencies have not set a participation goal. Such an estimate would enable Treasury and IRS to measure the tax credit’s participation rate, providing greater clarity regarding populations at risk of not receiving the payments. GAO recommends that Treasury, in coordination with IRS, estimate the number of individuals, includingnonfilers, who are eligible for advance CTC payments, measure the 2021 participation rate based on that estimate, and use that estimate to develop targeted outreach and communications efforts for the 2022 filing season; the participation rate could include individuals who opt in and out of the advance payments. Treasury neither agreed nor disagreed with this recommendation.

Child Nutrition

Child nutrition programs administered by the Department of Agriculture’s Food and Nutrition Service (FNS) supply cash reimbursements to schools or other programs for meals and snacks provided to eligible children nationwide. In fiscal year 2019, before the pandemic, the four largest programs—the National School Lunch Program, School Breakfast Program, Summer Food Service Program, and Child and Adult Care Food Program—along with other child nutrition programs, received $23.1 billion in federal funds. During a typical year, two of these programs—the National School Lunch Program and the School Breakfast Program—subsidize meals for nearly 30 million children in approximately 95,000 elementary and secondary schools nationwide.

As of July 2021, FNS officials were unable to provide a plan showing how FNS intends to comprehensively analyze lessons learned during the pandemic, such as from operational and financial challenges. Further, according to FNS officials, while the School Meals Operations study—launched in spring 2021—is surveying school districts and state agencies that administer the federal child nutrition programs, the study is not gathering local perspectives directly from child care centers and day care homes or other local program sponsors that are not school districts. As a result, FNS may miss opportunities to identify lessons learned and will lack comprehensive information to aid its future planning. GAO recommends that the Department of Agriculture document its plan to analyze lessons learned from operating child nutrition programs during the COVID-19 pandemic. This plan should include a description of how the department will gather perspectives of key stakeholders, such as Child and Adult Care Food Program institutions and nonschool Summer Food Service Program sponsors. The Department of Agriculture—which includes FNS—agreed with this recommendation.

Why GAO Did This Study

As of September 23, 2021, the U.S. had about 43 million reported cases of COVID-19 and about 699,000 reported deaths, according to CDC. The country also continues to experience economic repercussions from the pandemic.

Six relief laws, including the CARES Act, had been enacted as of August 31, 2021, to address the public health and economic threats posed by COVID-19. As of that same date (the most recent for which government-wide data was available), the federal government had obligated a total of $3.9 trillion and expended $3.4 trillion of the $4.8 trillion in COVID-19 relief funds that had been appropriated by these six laws, as reported by federal agencies.

The CARES Act includes a provision for GAO to report on its ongoing monitoring and oversight efforts related to the COVID-19 pandemic. This report examines the federal government’s continued efforts to respond to, and recover from, the COVID-19 pandemic.

GAO reviewed data, documents, and guidance from federal agencies about their activities. GAO also interviewed federal and state officials, stakeholders from organizations for localities, and other stakeholders.

Recommendations

GAO is making 16 new recommendations for agencies that are detailed in this Highlights and in the report.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Health Resources and Services Administration | The Administrator of the Health Resources and Services Administration should establish time frames for completing post-payment reviews to promptly address identified risks and identify overpayments made from the Provider Relief Fund, such as payments made in incorrect amounts or payments to ineligible providers. See the Relief for Health Care Providers enclosure. (Recommendation 1) |

HRSA partially concurred with this recommendation. In May 2023, HRSA provided us a summary of the post-payment reviews it has completed or planned to complete. All reviews were either completed or scheduled for completion. Additionally, in March 2023, HRSA established a process for reviewing payment irregularities and problematic payments. This process will address some of the issues originally identified for the post-payment review process. Given HRSA's completion of a schedule to complete post-payment reviews, we are closing this recommendation as implemented.

|

| Health Resources and Services Administration | The Administrator of the Health Resources and Services Administration should finalize procedures and implement post-payment recovery of any Provider Relief Fund overpayments, unused payments, or payments not properly used. See the Relief for Health Care Providers enclosure. (Recommendation 2) |

HRSA agreed with this recommendation. As of May 2023, HRSA had recovered more than $1 billion from providers. HRSA established a process to seek repayment from providers and refer to debt collection those providers who do not respond. In August 2023, HRSA established time frames for the recovery of all types of funds in need of recovery, including overpayments, unused payments, and payments not properly used. Based on GAO's review of HRSA's procedures for recovery, data on recoveries as of May 2023, and its planned schedule to seek recovery of all types of payments in need of recovery, GAO considers this recommendation closed.

|

| Department of the Treasury |

Priority Rec.

The Secretary of the Treasury should design and document timely and sufficient policies and procedures for monitoring recipients of Coronavirus State and Local Fiscal Recovery Funds to provide assurance that recipients are managing their allocations in compliance with laws, regulations, agency guidance, and award terms and conditions, including ensuring that expenditures are made for allowable purposes. See the Coronavirus State and Local Fiscal Recovery Funds enclosure. (Recommendation 3) |

Treasury agreed with the recommendation. As of September 2022, Treasury had designed and documented a risk-based compliance policy to monitor CLSFRF recipients' use of program funds and asserted that the agency would continue to adopt additional procedures as appropriate. Treasury's internal controls policies and procedures for monitoring recipients of CSLFRF awards are detailed in a suite of documents issued by the Office of Recovery Programs (ORP) including the Award Management Policy for Financial Assistance Recovery Programs; the Non-Compliance Determination Process for the State and Local Fiscal Recovery Funds Program; Project & Expenditure Report Compliance Matrices, Business Rules, and Data Analytics; Memorandum re: Q42021 P&E compliance approach; ORP Compliance Testing Procedures; and Recovery Plan Testing Procedures. Based on GAO's review of these documents, we consider this recommendation closed.

|

| Department of Labor | The Secretary of Labor should designate a dedicated entity and document its responsibilities for managing the process of assessing fraud risks to the unemployment insurance program, consistent with leading practices as provided in our Fraud Risk Framework. This entity should have, among other things, clearly defined and documented responsibilities and authority for managing fraud risk assessments and for facilitating communication among stakeholders regarding fraud-related issues. See the Unemployment Insurance Fraud Risk Management enclosure. (Recommendation 4) |

In January 2023, the Secretary of Labor designated the Department of Labor's (DOL) Chief Financial Officer (CFO) as the dedicated entity responsible for managing the process of assessing fraud risks to the unemployment insurance (UI) program. In April 2024, DOL told us that the UI Integrity Strategic Plan for fiscal year 2023-the most recent available at that time-establishes roles and responsibilities for those involved in UI fraud risk management. We reviewed this UI Integrity Strategic Plan. Specifically, it states that the Employment and Training Administration (ETA) provides guidance, technical assistance, funding and support to states combatting fraud, and assesses and addresses fraud risks, among other things. In addition, the 2023 UI fraud risk profile, provided by DOL in August 2023, states that ETA develops, updates, and oversees execution of the UI Integrity Strategic Plan, which continuously evolves and includes strategies to address emerging fraud threats and integrity risks to the UI program. Documenting the fraud risk management responsibilities for the UI program will help ensure appropriate oversight of the program.

|

| Department of Labor | The Secretary of Labor should identify inherent fraud risks facing the unemployment insurance program. See the Unemployment Insurance Fraud Risk Management enclosure. (Recommendation 5) |

In August 2023, DOL provided us with a copy of its UI fraud risk profile. This fraud risk profile identified 18 inherent fraud risks. The identified fraud risks include risks posed by claimants, employers, and state employees. Identifying inherent UI fraud risks will help provide DOL with key information to develop an antifraud strategy and effectively manage UI fraud risks.

|

| Department of Labor | The Secretary of Labor should assess the likelihood and impact of inherent fraud risks facing the unemployment insurance program. See the Unemployment Insurance Fraud Risk Management enclosure. (Recommendation 6) |

In August 2023, DOL provided us with a copy of its UI fraud risk profile. This fraud risk profile identified the significance, likelihood, and impact of each fraud risk. Assessing the likelihood and impact of inherent UI fraud risks will help provide DOL with key information to develop an antifraud strategy and effectively manage UI fraud risks.

|

| Department of Labor | The Secretary of Labor should determine fraud risk tolerance for the unemployment insurance program. See the Unemployment Insurance Fraud Risk Management enclosure. (Recommendation 7) |

In August 2023, DOL provided us with a copy of the 2023 UI fraud risk profile. However, the fraud risk profile did not specify the risk tolerance for individual inherent fraud risks or for UI overall. In August 2024, DOL provided us with the UI Integrity Strategic Plan for the second quarter of fiscal year 2024. In this plan, DOL stated that structural, programmatic, and operational challenges require the department to determine the UI program's fraud risk tolerance as "low". In September 2024, DOL officials provided us with an updated UI fraud risk profile, which included a priority ranking level and inherent risk likelihood and impact scores for each of the identified fraud risks. DOL officials also provided documentation describing how the priority ranking levels are connected to the department's risk tolerance. Determining and documenting its tolerance for UI fraud risks will help DOL ensure a consistent approach for developing an antifraud strategy and effectively managing UI fraud risks.

|

| Department of Labor |

Priority Rec.

The Secretary of Labor should examine the suitability of existing fraud controls in the unemployment insurance program and prioritize residual fraud risks. See the Unemployment Insurance Fraud Risk Management enclosure. (Recommendation 8) |

In August 2023, DOL provided us with a copy of the UI fraud risk profile. In this fraud risk profile, DOL identified the existing antifraud controls for each inherent risk listed on the fraud risk profile. DOL also identified the residual fraud risk for each inherent risk and prioritized them by very high, high, medium, and low. The residual risk designation on the fraud risk profile includes an explanation of the suitability of existing fraud controls. Examining the suitability of existing fraud controls and prioritizing residual fraud risks will help provide DOL with key information to develop an antifraud strategy and effectively manage UI fraud risks.

|

| Department of Labor | The Secretary of Labor should document the fraud risk profile for the unemployment insurance program. See the Unemployment Insurance Fraud Risk Management enclosure. (Recommendation 9) |

In August 2023, DOL provided us with a copy of the UI fraud risk profile. This fraud risk profile identified inherent risks to the UI programs and documents the significance, likelihood, and impact of each fraud risk. DOL also identified the residual fraud risk for each inherit risk included on the fraud risk profile. Documenting the fraud risk profile will help provide DOL with key information to develop an antifraud strategy and effectively manage UI fraud risks.

|

| Federal Emergency Management Agency | The Federal Emergency Management Agency Administrator should improve the consistency of the agency's interpretation and application of the COVID-19 Public Assistance policy within and across regions by further clarifying and communicating eligibility requirements nationwide. See the FEMA's Disaster Relief Fund and Assistance to State, Local, Tribal, and Territorial Governments enclosure. (Recommendation 10) |

In October 2021, the Department of Homeland Security (DHS) concurred with the recommendation and provided a number of steps it has taken. First, the Federal Emergency Management Agency (FEMA) has taken actions to improve consistent interpretation and application of COVID-19 Public Assistance (PA) policy nationwide. For instance, FEMA holds biweekly discussions with its Regional Recovery Division Directors and Regional PA Branch Chiefs that includes discussion on COVID-19 policy and needs facing localities across the nation. Second, FEMA issued recent policy updates--in May 2022, the agency provided guidance on its deadlines for COVID related-submissions, issued guidance in June 2022 on Air Disinfection eligibility, and is developing and implementing a national approach to addressing potential duplication of benefits between FEMA and patient care revenue slated to issue in fall 2022. Third, FEMA has conducted continued outreach to regions to further clarify and communicate eligibility requirements nationwide. PA leadership has held meetings, webinars, and/or trainings with PA staff to help ensure staff interpret and apply the COVID-19 policies consistently. Examples include-the eligibility of COVID-19 testing performed by the medical examiner's office on deceased individuals. Also, the eligibility of autopsy tools/equipment (May 2022); eligibility of at-home COVID-19 tests. (Discussions ongoing, clarification memo in draft); and eligibility of contract labor performed at private nonprofit hospitals; eligibility of backfill labor (April 2022). Finally, in August 2022, FEMA held a three-day in-person working session with 47 Headquarters staff, 30 FEMA regional staff, 58 representatives from states, territories, and tribes. The working session consisted of discussions on policy initiatives and a session devoted to COVID-19 policy implementation that included feedback/listening breakout sessions. As a result of these actions and evidence provided, we are closing as implemented.

|

| Federal Emergency Management Agency | The Federal Emergency Management Agency Administrator should require the agency's Public Assistance Program employees in the regions and at its Consolidated Resource Centers to attend training on changes to COVID-19 Public Assistance policy to help ensure it is interpreted and applied consistently nationwide. See the FEMA's Disaster Relief Fund and Assistance to State, Local, Tribal, and Territorial Governments enclosure. (Recommendation 11) |

In October 2021, FEMA concurred with the recommendation and stated that it took a number of actions to educate staff on changes to COVID-19 Public Assistance (PA) policy. For example, FEMA conducted a webinar with over 300 staff, which covered a number of issues. FEMA continues to address our recommendation by conducting webinars in 2022 and 2023 for State, Local, Tribal, and Territorial (SLTT) staff. The webinar topics included-Vaccine Administration in Grants Portal, COVID-19, Deadlines, and Duplications of Benefits. In addition, it held the Public Assistance Working Session with SLTT partners in 2022 and 2023. FEMA also told us that to ensure consistency, Regional PA Branch Chiefs' input was frequently sought as COVID specific policies and guidance were being developed by the HQ PA Division; such requests for input occurred informally and formally. These efforts led to a more consistent application of policies by sharing the same information with partners nationwide, who then shared that with their individual staff. Further, the PA Division conducts the "National Public Assistance Readiness Stand Down" training program. This program is a quarterly, all-hands training program which provides staff with current, critical updates to support the delivery of PA grants during current and future declared events; and serves as a main communication vehicle for consistent, universal messaging for all PA and to promote readiness for all disasters. FEMA provided GAO documentation of the topics covered and training materials. In November 2023, FEMA stated that the PA Division requires attendance by all invitees with limited exceptions. As a result of these actions, we consider this recommendation closed and implemented.

|

| Department of the Treasury | The Secretary of the Treasury should develop policies and procedures to determine when to act on warrants obtained as part of the loan program for aviation and other eligible businesses to benefit the taxpayers. See the Loans for Aviation and Other Eligible Businesses enclosure. (Recommendation 12) |

On March 22, 2023, Treasury provided GAO with its warrant policy and procedures document guide for determining when to act on the warrants it obtained from aviation businesses that participated in the Payroll Support Program and the Section 4003 loan program. In its guide, Treasury outlined various disposition procedures that it may recommend, the roles and responsibilities of Treasury units involved, portfolio management guiding principles for evaluating and recommending disposition activities, warrant monitoring, and the process for developing a disposition plan, among other things. By establishing this guide, Treasury is better positioned to act on warrants to help maximize the benefit to the federal government.

|

| Department of the Treasury | The Secretary of the Treasury should develop policies and procedures to determine when to act on warrants obtained as part of the Payroll Support Program to provide appropriate compensation to the federal government. See the Payroll Support Assistance to Aviation Businesses enclosure. (Recommendation 13) |

On March 22, 2023, Treasury provided GAO with its warrant policy and procedures document guide for determining when to act on the warrants it obtained from aviation businesses that participated in the Payroll Support Program and the Section 4003 loan program. In its guide, Treasury outlined various disposition procedures that it may recommend, the roles and responsibilities of Treasury units involved, portfolio management guiding principles for evaluating and recommending disposition activities, warrant monitoring, and the process for developing a disposition plan, among other things. By establishing this guide, Treasury is better positioned to act on warrants to help maximize the benefit to the federal government.

|

| Occupational Safety and Health Administration |

Priority Rec.

The Assistant Secretary of Labor for Occupational Safety and Health should assess—as soon as feasible and, as appropriate, periodically thereafter—various challenges related to resources and to communication and guidance that the Occupational Safety and Health Administration has faced in its response to the COVID-19 pandemic and should take related actions as warranted. See the Worker Safety and Health enclosure. (Recommendation 14) |

The Department of Labor (DOL) partially agreed with our recommendation. In September 2021, DOL stated that it agreed that it is important to assess lessons learned and best practices for the Occupational Safety and Health Administration's (OSHA) operational response to COVID-19. However, DOL officials said they believed that while the pandemic is ongoing, the agency's resources are best used to help employers and workers mitigate exposures to COVID-19. In December 2021, OSHA officials said they planned to conduct an assessment as soon as feasible, with a team of national office and field office staff, and would incorporate lessons learned, if applicable, into future emergency response efforts. In May 2022, OSHA officials said that the agency had taken a number of actions as a result of its ongoing assessment of successes and challenges during the pandemic, such as hiring new inspectors and implementing OSHA headquarters and field communication check-ins during periods of high COVID-19 transmission. In February 2023, OSHA officials said that, in fiscal year 2023, the agency would select and implement a task force to assess how OSHA could have improved its communications, provided clearer information, and sought feedback from the field in responding to the COVID-19 pandemic. In April 2024, OSHA officials said that, in fiscal year 2024, the agency would organize an internal group to produce a final report that includes actions OSHA could have taken to improve its response and communication during the pandemic, improvements OSHA has made, and actions OSHA plans to take during any future pandemic or national emergency. In September 2024, OSHA officials said a small OSHA steering group had developed an after-action report identifying areas for improvement and that the steering group would hold focus groups to discuss the after-action report with regional office managers and other OSHA directorates to capture positive and negative lessons learned, best practices, planning issues, training issues, and resource issues. In February 2025, OSHA officials said the agency is addressing internal comments on the draft after-action report. Officials said they anticipate finalizing the comments and presenting the report to OSHA leadership. We will close this recommendation when OSHA completes this assessment of the various challenges the agency faced in its response to the COVID-19 pandemic and has taken any related warranted actions.

|

| Department of the Treasury | The Secretary of the Treasury, in coordination with the Commissioner of Internal Revenue, should estimate the number of individuals, including nonfilers, who are eligible for advance child tax credit payments, measure the 2021 participation rate based on that estimate, and use that estimate to develop targeted outreach and communications efforts for the 2022 filing season; the participation rate could include individuals who opt in and out of the advance payments. See the Advance Child Tax Credit and Economic Impact Payments enclosure. (Recommendation 15) |

The Department of the Treasury neither agreed nor disagreed with this recommendation, stating in March 2022 that while it supports the goal of the recommendation, it has not estimated the eligible population for the advance child tax credit. Treasury also stated that it and IRS continue to undertake advance child tax credit outreach, education, and media campaign efforts. In March 2025, Treasury officials responded that the Department does not have any updates to this recommendation.

|

| Department of Agriculture | The Secretary of Agriculture should document the Department of Agriculture's plan to analyze lessons learned from operating child nutrition programs during the COVID-19 pandemic. This plan should include a description of how the department will gather perspectives of key stakeholders, such as Child and Adult Care Food Program institutions and nonschool Summer Food Service Program sponsors. See the Child Nutrition enclosure. (Recommendation 16) |

On March 31, 2023, FNS provided its plan for analyzing lessons learned from operating child nutrition programs during the COVID-19 pandemic. The plan included detailed information on how it would, or has, gathered perspectives of key stakeholders, such as Child and Adult Care Food Program institutions and nonschool Summer Food Service Program. For example, the plan includes data sources such listening sessions with tribal nutrition partners and Child and Adult Care Food Program sponsors and program operators; surveys of school food authorities; and interviews with state agencies. According to its plan, FNS will use these data sources to analyze internal processes and actions to understand how FNS responses during the COVID-19 pandemic impacted state and local program operators and program participants. FNS reported that it has begun to analyze the information gathered, and presented preliminary findings to Child Nutrition State agency staff in December 2022.

|