Temporary Assistance for Needy Families: HHS Needs to Strengthen Oversight of Single Audit Findings

Fast Facts

States get $16.5 billion a year in federal funding for the Temporary Assistance for Needy Families program.

States must audit their use of these funds and report the results to the Department of Health and Human Services. Recent audits found 162 deficiencies—56 of which were severe. For example, auditors found a state that didn't report required information for grants it gave with federal funds.

105 of the findings were similar to or the same as those in prior years' audits.

HHS must do more to help states address repeated findings, which could help ensure program funds are used for their intended purposes.

Our recommendations address this.

Highlights

What GAO Found

The Single Audit Act requires states and other entities that spend $1 million or more in federal awards each year to undergo a single audit. Single audits can help the Department of Health and Human Services (HHS) identify deficiencies in states' internal controls over financial reporting and over compliance requirements for federal award programs. Auditors report these deficiencies in single audit reports as audit findings.

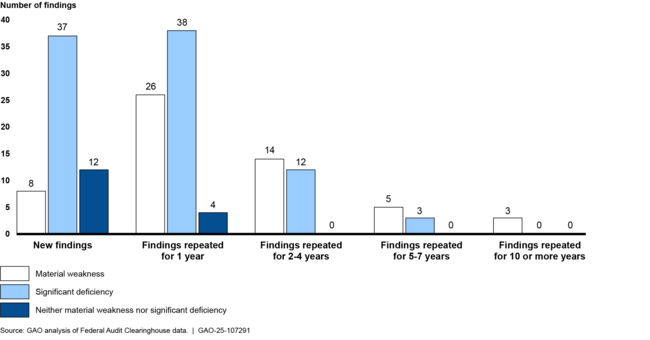

GAO identified 37 states with, collectively, 162 Temporary Assistance for Needy Families (TANF) audit findings in their single audit reports. Fifty-six of these findings were categorized as a material weakness, the most severe category of audit findings. For example, auditors found that one state did not report required information for awards granted to subrecipients. Thirty-seven of the 162 audit findings repeated for 2 or more years, and three remained unresolved for over a decade (see figure). Such findings—especially those categorized as material weaknesses—are considered particularly serious, as they can indicate critical risks and issues in a federal program. Additionally, some of these findings involved deficiencies that could lead to improper payments.

Number and Duration of Temporary Assistance for Needy Families Single Audit Findings, as of April 30, 2024

HHS's Administration for Children and Families (ACF), which administers the TANF block grant funds, has not updated its procedures for determining its effectiveness in helping states resolve TANF single audit findings. Additionally, ACF's procedures do not ensure that it issues timely management decisions to states. Management decisions are the agency's written evaluations of whether audit findings are sustained and the expected corrective actions to resolve the findings. Further, HHS does not have sufficient procedures to timely impose penalties on, or alternatively obtain corrective compliance plans from, states in violation of TANF program requirements. Developing effective procedures would better position HHS to help states improve internal controls over TANF federal awards and improve program outcomes.

Why GAO Did This Study

HHS annually provides about $16.5 billion in TANF grant funds to states to provide cash, supportive services, and non-cash assistance to low-income individuals and families with children. GAO was asked to review TANF spending and related control practices.

This report examines the nature and extent of TANF single audit findings, as of April 30, 2024, and the extent to which HHS has conducted oversight of TANF single audit findings, among other objectives. This report is part of a series of recent reports on TANF that GAO issued (GAO-25-107235, GAO-25-107290, and GAO-25-107226).

GAO reviewed states' timeliness in submitting 2023 single audit reports and identified the number of TANF-related findings and any commonalities in the most recent reports. GAO interviewed HHS officials and reviewed HHS policies and procedures for following up on TANF single audit findings; issuing management decisions; and imposing penalties on, or alternatively obtaining corrective compliance plans from, states that are not in compliance with TANF program requirements.

Recommendations

GAO is making three recommendations to HHS to (1) ensure that ACF updates its single audit resolution procedures, (2) ensure that ACF implements a strategy to issue management decisions timely, and (3) develop procedures to timely impose penalties, or alternatively obtain corrective compliance plans. HHS disagreed with the first recommendation; GAO clarified the procedures to be updated. HHS agreed with the second and partially agreed with the third recommendation

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Department of Health and Human Services | The Secretary of Health and Human Services should ensure that the Administration for Children and Families revises and implements its audit resolution standard operating procedures (dated November 2021) to include steps to track and measure the effectiveness of actions to help states resolve TANF single audit findings. (Recommendation 1) |

In its comments on our draft report, HHS disagreed with the recommendation. Administration for Children and Families (ACF) officials stated that it pertained to HHS's standard operating procedures (SOP), which was not written by ACF, and that implementing such procedures is at ACF's discretion. After receiving our draft report, ACF provided its own single audit resolution SOP. Therefore, we modified the recommendation to clarify that ACF, rather than HHS, should revise and implement its audit resolution SOP, or else it would not be able to determine how effective its processes are in helping to resolve findings and make any necessary adjustments for improvements. We will follow-up with HHS and ACF on actions to address this recommendation.

|

| Department of Health and Human Services | The Secretary of Health and Human Services should ensure that the Administration for Children and Families develops and implements a strategy to eliminate the accumulated TANF audit backlog, to ensure that management decisions are issued within the required time frame. (Recommendation 2) |

In its comments on our draft report, HHS agreed with this recommendation and suggested to specify that the backlog relates specifically to TANF findings, which we incorporated. HHS also cited actions that it has taken or will take to address it. We will follow-up with HHS on actions to address this recommendation.

|

| Department of Health and Human Services | The Secretary of Health and Human Services should develop, document, and implement additional procedures to timely impose penalties or alternatively obtain corrective compliance plans for states that are not meeting TANF program requirements. (Recommendation 3) |

In its comments on our draft report, HHS partially agreed with this recommendation. Specifically, HHS stated that it concurred with the portion of the recommendation to develop and implement additional procedures to timelier evaluate whether to impose penalties that do not relate to TANF work participation rates. However, it did not agree with the portion to document its determinations of whether to impose penalties for states that are not meeting TANF program requirements because its decisions to impose penalties were documented in penalty notification letters sent to the states. We reviewed the evidence HHS provided after receiving our draft report and found that while its decisions were documented, HHS does not have written procedures to do so timely. Therefore, we modified the recommendation to include written procedures to document decisions to impose penalties in a timely manner. We will follow-up with HHS on actions to address this recommendation.

|