Federal Reserve Lending Programs: Nearly Half of Main Street Program Loans Are Fully Repaid, but Losses Have Increased

Fast Facts

The Federal Reserve authorized 13 emergency lending programs in response to COVID-19, including the Main Street Lending Program. This program made 1,830 loans to small- and mid-sized businesses and nonprofits.

We found that as of August 31:

Almost half of the loans have been fully repaid

Less than 1% of current loans had late payments

About 8% of the loans had losses that totaled about $969 million

The Federal Reserve continues to regularly evaluate and issue internal reports on its processes related to the Main Street program.

Highlights

What GAO Found

In response to the COVID-19 pandemic, the Board of Governors of the Federal Reserve System authorized 13 emergency lending programs—known as facilities—to ensure the flow of credit across the economy. To improve oversight of these programs, the Federal Reserve issued seven reports from December 2020 through June 2024 that evaluated its internal processes and controls, such as for risk management and cybersecurity. These reports identified 20 opportunities to enhance internal controls. GAO found that Federal Reserve Banks, which manage the facilities, have fully addressed 19 of the 20 opportunities. The remaining opportunity, which relates to a facility's evaluation model that monitors loans' credit quality, is currently under review. GAO also found that the Federal Reserve's plans for ongoing monitoring of the facilities are generally aligned with federal internal control standards.

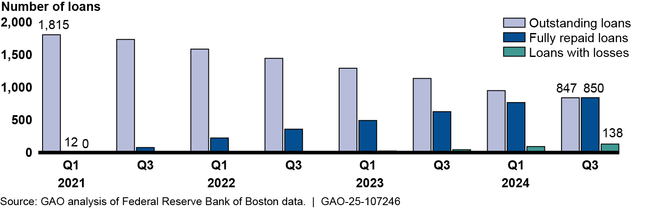

The five facilities under the Main Street Lending Program targeted small and midsize businesses and nonprofits. Of the 1,830 loans made through this program, 850 (or almost half) had been fully repaid as of August 31, 2024, the most recent data available. Further, 138 loans (or about 8 percent) had recorded a total of about $969 million in losses, a significant increase (about $781 million) year-over-year. About 46 percent (or 847 loans) remained outstanding. The program had collected about $1.89 billion in interest payments.

Main Street Lending Program Loans, First Quarter 2021–Third Quarter 2024

Note: Numbers may not add to the total number of loans due to varying loan statuses.

Loans to larger businesses have generally performed better than those to smaller ones. For example, businesses with annual revenues over $42.1 million at loan origination accounted for the largest share of repaid loans. In contrast, smaller businesses (annual revenues of $3.1 million or less) experienced higher rates of delinquencies and losses. Businesses in the construction sector have repaid a smaller proportion of loans and experienced higher delinquency rates compared with other sectors, such as the leisure and hospitality sector.

The higher rates of delinquencies and losses partly reflect the effects of higher interest payments and the 15 percent of each loan's principal that came due for borrowers in the second half of 2023. Interest rates higher than those at loan origination have increased borrowers' payments, potentially creating financial strain for businesses. Another 15 percent of each loan's principal came due during 2024, and a balloon payment of the remaining 70 percent will come due beginning mid-2025, potentially further affecting loan performance.

Why GAO Did This Study

As of the end of fiscal year 2024, four of the Federal Reserve's 13 lending facilities, all part of the Main Street Lending Program, continued to hold significant outstanding assets and loans. These facilities had approximately $4.7 billion in outstanding assets and loans, which will not mature until July 2025 or later. About $10.4 billion in collateral was pledged to secure the loans. The four facilities were among the nine that received funds appropriated through the CARES Act (section 4003). The Federal Reserve is required to monitor and report on the status of the facilities until they no longer hold outstanding assets or loans.

The CARES Act includes a provision for GAO to annually report on section 4003 loans, loan guarantees, and investments. This report examines (1) the Federal Reserve's oversight and monitoring of the CARES Act facilities and (2) the status and performance of Main Street Lending Program loans.

GAO reviewed Federal Reserve documentation, conducted loan-level analysis of Main Street Lending Program loan performance covering July 2020 through August 2024, and interviewed Federal Reserve officials.

For more information, contact Michael E. Clements at (202) 512-8678 or ClementsM@gao.gov.