DOD Financial Management: FY 2023 Financial Statement Audit Progress and Challenges

Fast Facts

We found that DOD made progress toward achieving a "clean" audit opinion in FY 2023—i.e., when auditors find that financial statements are presented fairly in accordance with accounting principles.

This Snapshot summarizes the progress DOD has made. For example, the Marine Corps received a "clean" opinion on its FY 2023 financial statements.

However, challenges remain. DOD's Office of Inspector General issued a disclaimer of opinion on DOD's department-wide financial statements, meaning they were unable to obtain sufficient, appropriate evidence on which to base an opinion.

Highlights

In fiscal year 2023, DOD reported total discretionary budget authority of $851.7 billion—about half of the federal government’s discretionary budget authority per the Office of Management and Budget—and total assets of $3.8 trillion. As stated in our April 2023 High Risk report, DOD financial management and business systems modernization face long-standing issues, including ineffective processes, systems, and controls. While DOD has made progress in addressing its financial management challenges, achieving a “clean” audit opinion on its department-wide financial statements has eluded it.

The Big Picture

In fiscal year (FY) 2023, the Department of Defense (DOD) continued making progress toward its goal to achieve an unmodified (or “clean”) audit opinion, which is when auditors conclude that financial statements are presented fairly in accordance with generally accepted accounting principles. For example, the Marine Corps received a clean audit opinion on its FY 2023 financial statements, reflecting significant progress for DOD.

However, DOD’s Office of Inspector General issued a disclaimer of opinion on DOD’s department-wide financial statements, meaning it was unable to obtain sufficient, appropriate evidence on which to base an opinion.

In May 2023, we reported that the financial statement audit process has been valuable—providing tangible short- and long-term benefits. DOD noted:

➢ Audits have helped identify assets it did not know existed. For example, in FY 2020, the Navy identified and added nearly $2.4 billion of unrecorded inventory, operating materials and supplies, and general equipment to its records.

➢ Audits have improved DOD’s oversight and efficiency in processing financial transactions. For example, in FY 2022, the Air Force identified and corrected approximately $5.2 billion worth of discrepancies in its accounts.

➢ Audits have led to better management of funding obligations. For example, DOD identified $43 million in contract deobligations in 2022, allowing it to reprogram the funds for more immediate needs.

What GAO’s Work Shows

For FY 2023, along with DOD’s department-wide disclaimer of opinion, DOD’s auditors reported that 18 of 29 components received disclaimers—including the Army, Navy, and Air Force—while 10 of DOD’s components—including the Marine Corps—received clean audit opinions (see table 1).

Table 1: Results for DOD Components Undergoing Stand-alone Audits, Fiscal Years (FY) 2023 and 2022

|

Audit opinion |

FY 2023 |

FY 2022 |

|

Unmodified or “clean”a |

10 |

9 |

|

Qualifiedb |

1 |

1 |

|

Disclaimerc |

18 |

16 |

|

Totald |

29 |

26 |

Source: GAO, DOD. | GAO-24-107478

Notes: GAO analysis of data from the FY 2023 and 2022 agency financial reports (AFR) of Department of Defense (DOD), Defense Information Systems Agency’s Working Capital Fund, and the DOD Inspector General; the Marine Corps’ FY 2023 AFR; and GAO-23-105784.

aAn unmodified (or “clean”) opinion is when the auditor concludes that financial statements are presented fairly in accordance with U.S. generally accepted accounting principles.

bA qualified opinion is when the auditor can express an opinion on the financial statements except for specific areas where material misstatements exist but are not pervasive or where auditors were unable to obtain sufficient, appropriate evidence, but the possible effects are not pervasive.

cA disclaimer of opinion is when auditors were unable to obtain sufficient, appropriate evidence to provide an opinion on the financial statements.

dThe Marine Corps General Fund was not audited in FY 2022. Also, the number of DOD components undergoing stand-alone audits increased from FY 2022.

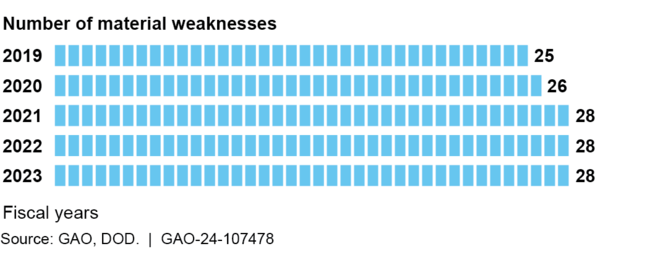

Auditors also report on identified material weaknesses in internal controls. For FY 2023, DOD’s department-wide auditor reported that DOD had 28 material weaknesses, which increased since 2019 (see fig. 1). A material weakness is a deficiency in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected, on a timely basis.

Figure 1: Department of Defense (DOD) Material Weaknesses, Fiscal Years 2019 through 2023

Note: GAO analysis of DOD’s fiscal year 2023 agency financial report and GAO-23-105784.

Some of the increases in material weaknesses may be due to more of DOD’s components and entities being audited. In May 2023, we recommended that DOD develop a comprehensive plan with detailed procedures for addressing material weaknesses to help DOD reach its goal of achieving a clean audit opinion.

DOD reported that for FY 2023, the Secretary of Defense prioritized efforts to address certain widespread material weaknesses, including issues related to Fund Balance with Treasury (FBWT). DOD has been unable to reconcile its FBWT accounts—a process similar to reconciling a checkbook to a bank statement. Although the DOD department-wide FBWT material weakness persisted for the 6th straight year in FY 2023, DOD’s auditors reported that certain components had their FBWT material weakness reduced to a significant deficiency (less severe than a material weakness)—the Army’s Working Capital Fund ($3.5 billion FBWT) and the Navy’s General Fund ($219.8 billion FBWT)—or resolved—the Air Force’s General Fund ($184.1 billion FBWT).

Challenges and Opportunities

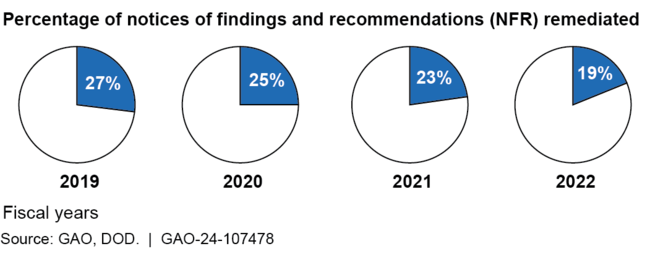

As part of the audit process, DOD’s auditors issue notices of findings and recommendations (NFR) that inform DOD of issues identified during the audit. In May 2023, we reported that DOD’s remediation rate for fully resolving NFRs decreased from FY 2019 to 2022 (see fig. 2). According to DOD officials, this is because it initially addressed less-complex issues identified in NFRs; more complex issues can take multiple years to resolve.

Figure 2: Department of Defense (DOD) NFR Trends, Fiscal Years 2019 through 2022

Note: GAO analysis of DOD’s fiscal year NFR data from GAO-23-105784.

We also tracked GAO financially related open public recommendations targeted to DOD per our Recommendations Database since 2013. The database covers FY 2002 to the present and is updated daily. As of May 28, 2024, for an agency search on “Department of Defense” and a topic search on “Auditing and Financial Management,” 53 recommendations remain open, including nine priority recommendations.

Information included in this product was summarized from GAO-16-47, GAO-22-105894, GAO-23-105784, GAO-23-106203, GAO-24-106660, and GAO’s public Recommendations Database, as well as FY 2023 and 2022 agency financial reports (AFR) for DOD, the Defense Information Systems Agency’s Working Capital Fund, and the DOD Inspector General; the FY 2023 Army Annual Financial Report; the FY 2023 AFRs for the Navy, Air Force, and Marine Corps; DODIG-2023-070; and Office of Management and Budget’s Historical Tables (Table 5.6 - Budget Authority for Discretionary Programs).

For more information, see:

https://www.gao.gov/

https://comptroller.defense.gov/ODCFO/afr/

https://www.dodig.mil/reports.html/

https://www.whitehouse.gov/omb/budget/historical-tables/

For more information, contact Asif Khan, Director, Financial Management & Assurance at (202) 512-9869 or KhanA@gao.gov.