Hospital Financing: Volume Limits and Reporting Could Help Manage Risks of Expanding FHA's Mortgage Insurance Program

Fast Facts

The Federal Housing Administration insures mortgage loans to hospitals that need financing for projects like renovations. The insurance protects lenders from losses if hospitals don't make their loan payments.

Currently, hospitals that provide acute care—like emergency services—are eligible. We looked at the potential effects of expanding the program to others, such as psychiatric hospitals. These hospitals generally have less revenue, which may increase FHA's risk if it insures their loans.

If Congress expands the program, it may wish to consider our recommendations for managing risks—like initially limiting how many new loans FHA insures.

Highlights

What GAO Found

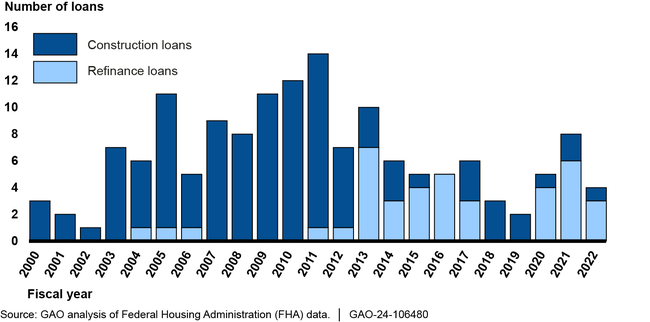

The Federal Housing Administration's (FHA) Hospital Mortgage Insurance Program insures loans for capital improvements at hospitals that primarily provide general acute care services. The number and types of loans FHA insured annually varied in fiscal years 2000–2022, partly in response to economic conditions and program expansions. For example, program use temporarily increased in 2009 following creation of the Build America Bonds program (which incentivized infrastructure projects) and in 2013 following a program expansion that codified certain options to refinance non-FHA-insured debt.

Number of New Hospital Mortgage Loans Insured Annually by FHA, by Loan Type, Fiscal Years 2000–2022

Hospital types generally ineligible for FHA's program, such as psychiatric and long-term care hospitals, have characteristics that can limit their financing options or increase financing costs compared to eligible hospital types. They are generally smaller facilities and have lower average revenues and profit margins than eligible hospital types. Hospitals with smaller revenue bases and weaker financial performance may have difficulty qualifying for affordable loans or securing public credit ratings needed to issue bonds.

Extending the program to ineligible hospitals could increase program participation and risks, but specific effects are difficult to estimate. GAO estimates that about 2,600 additional hospitals could become eligible, but the number that could meet FHA's underwriting standards is unknown, and some characteristics of these hospitals could add uncertainty to FHA's underwriting process. For example, less predictable revenue sources at some psychiatric hospitals could challenge FHA's ability to estimate long-term default risks. Prior practices Congress has used to manage FHA program risks may be applicable to expanding the hospital program. These include initially limiting the volume of new loans and requiring FHA to regularly report on program activity, including the performance of new loans. Such practices would help ensure that program risks related to an expansion were effectively monitored, controlled, and evaluated.

Why GAO Did This Study

FHA's Hospital Mortgage Insurance Program currently insures more than $6 billion in loans for the expansion and renovation of hospitals that provide general acute care services, such as surgeries and treatments for injuries and short-term illnesses. Legislation introduced but not enacted in the 117th Congress proposed extending eligibility to hospitals that primarily provide non-acute care services, such as treatment of mental health disorders.

GAO was asked to evaluate the potential effects of expanding program eligibility. This report examines (1) use of the program from fiscal years 2000–2022, (2) characteristics of ineligible hospital types that may affect their financing options, and (3) the potential effects of extending eligibility on program participation and risks.

GAO analyzed FHA documents and data for fiscal years 2000–2022; hospital financial data from the Centers for Medicare & Medicaid Services for 2016–2020 (the most recent available year); and industry, academic, and government reports. GAO also interviewed representatives from FHA, lenders, mental health providers, appraisers, and hospital and health care associations.

Recommendations

If Congress decides to expand program eligibility, it should consider adopting practices to help manage potential risks. These could include initially limiting the volume of loans to new hospital types and requiring FHA to regularly report on new program activity. FHA did not have any comments on the report.

Matter for Congressional Consideration

| Matter | Status | Comments |

|---|---|---|

| Congress should consider, if it decides to expand eligibility for FHA's Hospital Mortgage Insurance Program by eliminating the patient-day requirement, adopting practices to help manage risks to the program. For example, Congress could consider (1) requiring FHA to regularly report on program activity, including the number, characteristics, and performance of insured loans to newly eligible hospital types and (2) limiting the volume of insured loans to newly eligible hospital types, such as through a pilot program, and requiring FHA to evaluate lessons learned before easing volume restrictions. (Matter for Consideration 1) | As of March 2024, Congress had not acted on this matter for consideration. |