Single Audits: Improving Federal Audit Clearinghouse Information and Usability Could Strengthen Federal Award Oversight

Fast Facts

Federal award amounts distributed to recipients have increased substantially since the onset of the COVID-19 pandemic.

If an award recipient spends $750,000 or more in federal funds in a year, it must undergo an audit of its award spending. The results of this "single audit" must be submitted to the Federal Audit Clearinghouse, which is maintained by the General Services Administration.

We found issues with the quality and completeness of the data in this clearinghouse. For example, the clearinghouse can't identify recipients that are required to submit a single audit but didn't.

We recommended, among other things, that GSA address this issue.

Highlights

What GAO Found

The Single Audit Act requires nonfederal entities that spend $750,000 or more in federal awards in a year to undergo a single audit, which is an audit of an entity's financial statements and federal awards, or in select cases a program-specific audit, and submit the results to the Federal Audit Clearinghouse (FAC). The U.S. Census Bureau maintained the FAC until October 2023, when the Office of Management and Budget (OMB) designated the General Services Administration (GSA) to assume responsibilities.

GAO identified some issues with FAC processes that affect the reliability and usefulness of single audit information. For example, the FAC currently cannot identify recipients that should have submitted a single audit but did not. As a result, federal agencies may not have all the data they need to conduct oversight. In addition, OMB has not designated an entity to conduct a government-wide single audit quality review since 2007. Given the trillions of dollars of COVID-19-related financial assistance provided in recent years, a government-wide review is increasingly important to help identify issues in the quality of single audits that can lead to unreliable FAC information.

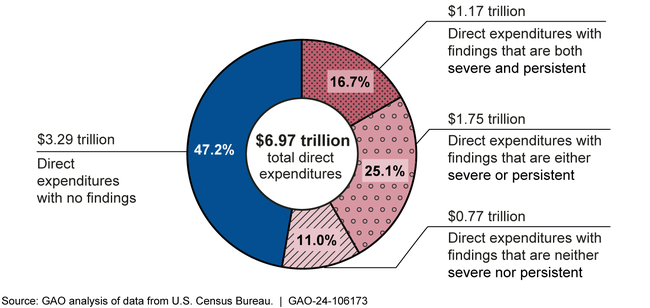

GAO also found that $1.17 trillion of the reported $6.97 trillion of direct federal award funds spent by recipients from 2017 through 2021 were linked to single audit findings that were both severe (contributed to an auditor's modified opinion or material weakness) and persistent (repeated over multiple years).

Severity and Persistence of Single Audit Findings by Direct Expenditure of Federal Awards, 2017-2021

Note: Numbers may not sum due to rounding. For more details, see fig. 4 in GAO-24-106173.

These findings were also related to $69 billion of COVID-19 relief funds spent from 2020 to 2021. GAO identified 213 findings reported in 2015 or earlier that remained unresolved in 2021.

Why GAO Did This Study

Federal award amounts distributed to recipients have increased substantially since the onset of the COVID-19 pandemic. For fiscal year 2023, $1.1 trillion of awards were distributed and about 40,000 single audits were submitted to the FAC. Single audits are an important tool to help ensure that award recipients are complying with the requirements of their awards.

The CARES Act includes a provision for GAO to conduct oversight of funds made available to respond to the COVID-19 pandemic. This report examines (1) FAC data reliability for oversight purposes, including oversight of COVID-19 relief funding; (2) processes involved in using and overseeing the FAC; and (3) the extent to which federal award expenditures were linked to severe and persistent single audit findings reported in the FAC.

GAO analyzed FAC data from 2015 through 2021 (the most recent complete data available at the time of review). GAO interviewed selected federal agencies and audit community members about their use of the FAC.

Recommendations

GAO is recommending three matters for Congress to consider, including amending the Single Audit Act to require OMB to initiate a government-wide single audit quality review at a regular interval.

GAO is making 10 recommendations, including four to GSA and six to OMB, to implement guidance and other strategies to further enhance the use and oversight of the FAC. GSA and OMB agreed with GAO's recommendations to them.

Matter for Congressional Consideration

| Matter | Status | Comments |

|---|---|---|

| Congress should consider amending the Single Audit Act to require the Director of OMB to initiate a government-wide single audit quality review at a regular interval, such as the 6 years that the Uniform Guidance recommends. (Matter for Consideration 1) | Congress drafted provisions incorporating this matter in the Financial Management Risk Reduction Act (P.L. 118-207), which was signed into law on December 23, 2024. | |

| Congress should consider amending the Single Audit Act to require the Director of OMB to submit a report on the findings from each government-wide single audit quality review to the appropriate committees of Congress. (Matter for Consideration 2) | Congress drafted provisions incorporating this matter in the Financial Management Risk Reduction Act (P.L. 118-207), which was signed into law on December 23, 2024. | |

| Congress should consider amending the Single Audit Act to require the federal awarding agencies to work with the Director of OMB on a government-wide single audit quality review. (Matter for Consideration 3) | Congress drafted provisions incorporating this matter in the Financial Management Risk Reduction Act (P.L. 118-207), which was signed into law on December 23, 2024. |

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| General Services Administration |

Priority Rec.

The Administrator of GSA should develop a process to regularly identify, analyze, and respond to FAC data reliability issues that may affect federal oversight, such as establishing edit checks to mitigate issues related to data accuracy, consistency, and completeness. (Recommendation 1) |

In response to our recommendation, GSA developed standardized processes in September 2025 to respond to data reliability issues by allowing Federal Audit Clearinghouse (FAC) users to request corrections to ensure the accuracy of the data elements, such as unique entity identifiers and program names. GSA's actions should help improve the reliability of FAC data, thereby also improving federal agencies' oversight of federal award spending.

|

| General Services Administration |

Priority Rec.

The Administrator of GSA should, in coordination with federal agencies and professional audit organizations, identify and prioritize features to enhance the usefulness of FAC data for federal oversight in accordance with federal data standards. (Recommendation 2) |

In response to our recommendation, GSA solicited the FAC Advisory Committee's feedback and, in January 2026, began meeting regularly with federal and state Federal Audit Clearinghouse (FAC) users and audit community members to share updates, conduct demonstrations, answer questions, and gather user feedback on priorities to guide planning. GSA also established two working groups to improve the data collection form and help ensure accurate audit resubmissions. Further, in collaboration with the National Association of State Auditors, Comptrollers and Treasurers, GSA created draft analytics on FAC.gov to enhance federal oversight and created a dashboard for FAC users to track their audits. GSA's actions to identify, prioritize, and implement enhanced FAC features should help make single audit information more useful and improve federal award oversight.

|

| General Services Administration |

Priority Rec.

The Administrator of GSA should, in coordination with federal agencies, develop proposed funding and timelines for implementing the identified and prioritized features to enhance the usefulness of FAC data for federal oversight through interagency agreements or other methods. (Recommendation 3) |

GSA agreed with this recommendation. To identify funding for implementing new features for FAC data, GSA developed a methodology to determine federal agencies' contributions to funding the FAC for fiscal years 2025 and 2026. Further, in April 2025, GSA provided its planned fiscal year 2026 budget for the FAC and a roadmap for enhancing the usefulness of FAC data. However, GSA officials stated that planned reductions to GSA's workforce will significantly impact the FAC's funding and timelines for enhancements. In December 2025, GSA officials stated that, as part of its August 2025 FAC Advisory Committee meeting, GSA provided information to agency stakeholders regarding the budget allocation calculation, fiscal year 2026 contributions per agency, and anticipated fiscal year 2027 contributions and will continue to discuss prioritizing FAC features with stakeholder input. To fully implement this recommendation, GSA needs to coordinate with federal agencies to develop and document proposed funding and timelines for implementing features in the FAC. Doing so would help GSA in allocating its resources for improving the FAC. We will continue to follow-up with GSA on actions to address this recommendation.

|

| Office of Management and Budget | The Director of OMB should, after consultation with federal agencies, implement the government-wide single audit quality review by naming a federal agency to lead the review as required by the Uniform Guidance. (Recommendation 4) |

OMB agreed with this recommendation. In response to our follow-up on actions to address this recommendation, in March 2025, OMB told us it has no updates to provide. As of mid-February 2026, OMB had not provided additional information about the implementation status of this recommendation. We will continue to follow-up with OMB on actions to address this recommendation.

|

| Office of Management and Budget | The Director of OMB should ensure that each of the federal agencies responsible for single audit oversight (cognizant and oversight agencies for audit) collects and reports to GSA a list of the recipients of its federal awards that should have submitted a single audit report for audit year 2023 and did not. (Recommendation 5) |

OMB agreed with this recommendation. In response to our follow-up on actions to address this recommendation, in March 2025, OMB told us it has no updates to provide. As of mid-February 2026, OMB had not provided additional information about the implementation status of this recommendation. We will continue to follow-up with OMB on actions to address this recommendation.

|

| Office of Management and Budget | The Director of OMB should work with the Administrator of GSA to establish formal guidance implementing an annual process for each of the federal agencies to collect and report to GSA a list of its federal award recipients that should have submitted a single audit report and did not and to then communicate the guidance to federal agencies for single audits in 2024 and beyond. (Recommendation 6) |

OMB agreed with this recommendation. In response to our follow-up on actions to address this recommendation, in March 2025, OMB told us it has no updates to provide. As of mid-February 2026, OMB had not provided additional information about the implementation status of this recommendation. We will continue to follow-up with OMB on actions to address this recommendation.

|

| Office of Management and Budget | The Director of OMB should work with the Administrator of GSA to develop a method for determining federal award recipients that did not submit a single audit report but should have based on their combined funds received from multiple federal agencies and communicate this method to federal awarding agencies. (Recommendation 7) |

OMB agreed with this recommendation. In response to our follow-up on actions to address this recommendation, in March 2025, OMB told us it has no updates to provide. As of mid-February 2026, OMB had not provided additional information about the implementation status of this recommendation. We will continue to follow-up with OMB on actions to address this recommendation.

|

| General Services Administration |

Priority Rec.

The Administrator of GSA should, upon consulting with professional audit organizations, provide additional training to auditors and recipients to help ensure that they complete FAC data collection forms accurately, completely, and consistent with the audit report. (Recommendation 8) |

GSA agreed with this recommendation. As of April 2026, GSA has standing meetings to communicate with federal and state agency Federal Audit Clearinghouse (FAC) stakeholders on at least a monthly basis to collect feedback. GSA also created a working group with federal agency FAC users to recommend improvements to the content of its FAC data collection form; however, no changes have yet been implemented. In addition, GSA provided a fiscal year 2026 roadmap which includes plans to rebuild and refine training resources. However, GSA has not provided any details on what this entails. Previously, in April 2025, GSA officials stated that GSA had planned to provide training but cancelled the training because it coincided with the organization-wide pause in external communications. To fully implement this recommendation, GSA needs to develop a documented process for providing additional training to recipients and auditors on any updates to guidance for completing FAC data collection forms. Doing so would ensure that information in the FAC is accurate and complete. We will continue to follow-up with GSA on actions to address this recommendation.

|

| Office of Management and Budget | The Director of OMB should consult with federal agencies, CIGIE, and relevant OIGs to discuss methods to help ensure that single audit report reviewers are verifying that the information in a single audit report aligns with the summary information entered on the FAC data collection form. These methods could include adding a procedure to conduct a final quality check in CIGIE's Guide for Desk Reviews of Single Audit Reports. (Recommendation 9) |

OMB agreed with this recommendation. In response to our follow-up on actions to address this recommendation, in March 2025, OMB told us it has no updates to provide. As of mid-February 2026, OMB had not provided additional information about the implementation status of this recommendation. We will continue to follow-up with OMB on actions to address this recommendation.

|

| Office of Management and Budget | The Director of OMB should work with GSA and agency key management single audit liaisons to develop a strategy to use FAC data to identify government-wide risks to federal award funds, such as single audit reports that contain findings that are severe or have remained unresolved for multiple years. This strategy should include steps to analyze and respond to significant risks identified. (Recommendation 10) |

OMB agreed with this recommendation. In response to our follow-up on actions to address this recommendation, in March 2025, OMB told us it has no updates to provide. As of mid-February 2026, OMB had not provided additional information about the implementation status of this recommendation. We will continue to follow-up with OMB on actions to address this recommendation.

|