DOD Financial Management: Additional Actions Would Improve Reporting of Joint Strike Fighter Assets

Fast Facts

Department of Defense auditors found issues with how DOD reports certain assets in its financial statements for the Joint Strike Fighter program—its most costly weapon system in history. DOD hasn't fully developed a strategy to address the reporting issues. It has also struggled with following procedures for inventorying all program assets, like those held by contractors.

As a result, DOD can't ensure that it has current records on all of the program assets that it owns, where they are located, and how much they cost. Without these records, DOD won't have data needed for reliable financial reporting. We recommended that DOD address these issues.

F-35 Joint Strike Fighter

Highlights

What GAO Found

The Department of Defense (DOD) has taken steps to address the material weakness that auditors identified related to the F-35 Joint Strike Fighter (JSF) program, including establishing milestone dates for addressing underlying issues. However, GAO found that because it lacks a fully developed strategy, DOD has not met and subsequently revised the milestone dates. Without a documented strategy that includes detailed procedures for addressing the material weakness, DOD is at an increased risk that its effort to remediate the JSF financial reporting issues will not meet milestone target dates and will not be effective.

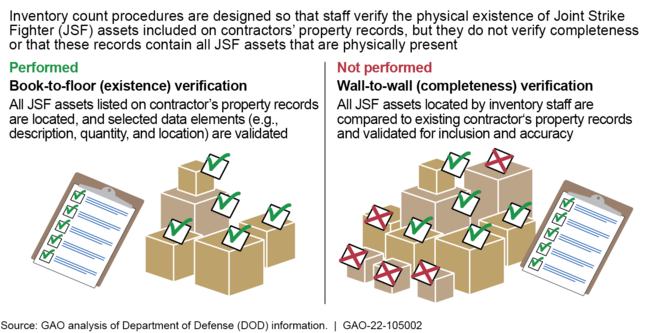

Further, GAO found that DOD designed inventory count procedures to verify the physical existence of certain JSF assets such as support equipment held at contractor facilities and included in property records; however, DOD did not verify the completeness of assets, as directed by DOD guidance (see figure).

DOD Inventory Count Procedures of Joint Strike Fighter Assets

Because DOD had never previously maintained its own complete JSF property records, it relied on contractor records to perform the inventory, but these sometimes were inaccurate. For example, DOD was unable to verify approximately $16 million of JSF assets listed on contractor records. DOD officials said that these errors are likely to be significantly higher. Without properly executed inventory procedures that verify both the physical existence of the assets and the completeness of the records, DOD management will not have the information needed for reliable financial statement reporting and may not be able to identify if assets have been lost or stolen.

DOD was unable to provide complete and consistent information about the universe of DOD joint programs. This limited GAO's ability to fully examine and determine the extent to which DOD tracks and records information about its joint programs. GAO found inconsistencies in DOD's reported data about its joint programs and in how DOD offices define and identify joint programs. This increases the risk that financial data used for managing and reporting joint programs will not be consistent, complete, or accurate.

Why GAO Did This Study

In fiscal year 2019, DOD auditors identified a material weakness related to the JSF program. The JSF is DOD's most costly weapon system in history, with overall costs estimated to be more than $1.7 trillion over the program's life cycle. Auditors reported that DOD did not report certain JSF program's assets on its financial statements. This omission, as well as DOD's inability to provide supporting documentation for the value of the assets, indicated material failures in controls for recording joint programs at DOD.

This report, developed in connection with fulfilling GAO's mandate to audit the U.S. government's consolidated financial statements, examines the extent to which DOD (1) has developed and implemented procedures for addressing the material weakness and (2) tracks and records information about its joint programs.

GAO reviewed, among other things, relevant reports and accounting standards, JSF documents, and DOD policies and procedures; interviewed DOD officials; and conducted site visits at three contractors' locations.

Recommendations

GAO is making 12 recommendations, including for DOD to develop and document a strategy to address the material weakness and plans to verify the completeness of JSF asset records, and to determine whether information on joint programs is sufficiently maintained for reporting purposes. DOD concurred with 10 and partially concurred with two of GAO's recommendations. GAO continues to believe that all the recommendations are warranted.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Department of Defense |

Priority Rec.

The Under Secretary of Defense for Acquisition and Sustainment together with the F-35 Program Executive Officer, and in coordination with the Under Secretary of Defense (Comptroller), should develop and document a comprehensive strategy to address the JSF material weakness. The strategy should include (1) complete, detailed procedures; (2) time frames based on an analysis of the time needed to accomplish the procedures; and (3) resources required to design and implement the procedures. (Recommendation 1) |

The Department of Defense (DOD) concurred with this recommendation. In response to our recommendation, in September 2023, the Office of the Under Secretary of Defense for Acquisition and Sustainment issued the F-35 Joint Strike Fighter Financial Reporting Strategy to manage accountability and reporting of Joint Strike Fighter assets to address the material weakness. The Strategy describes detailed procedures which include time frames for the expected duration of each procedure. Additionally, in August 2022, the F-35 Joint Program Office conducted a manpower study to determine the resources necessary to operate the accountable property system of record that will be used to manage Joint Strike Fighter assets. If fully and effectively implemented, this strategy will increase the likelihood that efforts to remediate the material weakness will meet milestone target dates.

|

| Department of Defense |

Priority Rec.

The Under Secretary of Defense for Acquisition and Sustainment together with the F-35 Program Executive Officer should develop and document a plan for verifying the completeness of JSF assets recorded in its APSR, including conducting an analysis and documenting the results on the feasibility of performing a wall-to-wall inventory to capture all JSF assets. (Recommendation 2) |

The Department of Defense (DOD) concurred with this recommendation. In response to our recommendation, in July 2024, the F-35 Joint Program Office issued the Defense Property Accountability System Internal Oversight Validation Guidebook, which describes procedures on conducting (1) reviews of physical inventory results and (2) sample selections to validate the accuracy and completeness of records in its accountable property system of record. Also, the January 2023 version of the F-35 Joint Program Office Physical Inventory Plan includes guidance that inventories are not completed until they are reconciled to the records in the accountable property system of record. As DOD elected to perform a 100 percent wall-to-wall physical inventory of JSF assets, it forewent the feasibility analysis. If fully and effectively implemented, the measures DOD has put in place will enable it to ensure that the Joint Strike Fighter asset records are accurate, thereby decreasing the risk of misstatement in DOD's financial statements.

|

| Department of Defense | The Under Secretary of Defense for Acquisition and Sustainment together with the F-35 Program Executive Officer should develop procedures for performing physical inventories of JSF assets held at DOD and international partner facilities. To the extent that the procedures include the F-35 JPO relying on these facilities' staff to perform the physical inventory counts, the office should develop and document a plan that describes how the F-35 JPO plans to review the results of these inventory procedures in order to verify the existence and completeness of the recorded amounts of JSF assets at these locations. (Recommendation 3) |

Department of Defense (DOD) concurred with this recommendation. In response to our recommendation, in January 2023, DOD issued the F-35 Joint Program Office (JPO) Physical Inventory Plan that requires F-35 non-contractor sites to follow procedures for performing physical inventories listed in the F-35 JPO Sustainment Supply User Guide. Also, in July 2024, the F-35 JPO issued the Defense Property Accountability System Internal Oversight Validation Guidebook, which describes how the F-35 JPO will conduct oversight validation to ensure accuracy and completeness of Joint Strike Fighter asset records, to include non-contractor locations. If fully and effectively implemented, DOD's procedures for inventory and oversight will enable it to ensure that the Joint Strike Fighter inventory count is accurate, better identify if assets are lost or stolen, and decrease the risk of making unnecessary purchases.

|

| Department of Defense | The Under Secretary of Defense for Acquisition and Sustainment together with the F-35 Program Executive Officer should develop procedures for performing periodic physical inventories once the initial inventory count has been completed, including how DOD will assess the resources and time needed to conduct the inventories and any sampling methodology intended to be used. (Recommendation 4) |

DOD concurred with this recommendation and stated that under the guidance of the Office of the Under Secretary of Defense for Acquisition and Sustainment (OUSD(A&S)), the F-35 Joint Program Office (JPO) is currently developing policies and procedures for both regularly scheduled inventory verification and sampling methodologies. These policies and procedures will include addressing the resources and time needed to conduct the inventories. The estimated completion date for developing policies and procedures was June 30, 2024. We followed up with DOD multiple times regarding the status of the recommendation. In July 2025, our DOD point of contact told us they are working with OUSD A&S and JPO to obtain an update and will notify us once it is received. We will continue to follow-up on the status of this recommendation.

|

| Department of Defense |

Priority Rec.

The Under Secretary of Defense for Acquisition and Sustainment together with the F-35 Program Executive Officer should develop procedures that outline the steps to periodically capture and verify the accuracy and completeness of JSF asset data from contractors and other DOD sources to be recorded in DPAS until a direct interface with the prime contractors' systems has been established. (Recommendation 5) |

DOD concurred with this recommendation. The F-35 Joint Program Office (JPO) has been coordinating with the OUSD(A&S) and the Defense Logistics Agency since fiscal year 2019 to implement the program's accountable property system of record, Defense Property Accountability System (DPAS). With guidance from the OUSD(A&S), the JPO is in the process of developing procedures for periodic capture, validation, and upload into DPAS of property data from contractor and DOD sources. The periodic data management processes will support F-35 property accountability until a direct IT system interface, or other DOD-approved solutions are established. As of January 2025, the expected date of completion for these actions was June 30, 2025. We followed up with DOD multiple times regarding the status of the recommendation. In July 2025, our DOD point of contact told us that they are working with OUSD A&S and JPO to obtain an update and will notify us once it is received. We will continue to follow-up on the status of this recommendation.

|

| Department of Defense | The Under Secretary of Defense for Acquisition and Sustainment together with the F-35 Program Executive Officer should finalize the business rules within DPAS to identify and populate default characters for missing data elements in JSF asset property records. (Recommendation 6) |

DOD concurred with this recommendation and stated that the F-35 Joint Program Office (JPO) has drafted business rules to identify and populate values for missing mandatory data elements where gaps exist in the Joint Strike Fighter (JSF) property data currently available from contractors and DOD sources. JPO will coordinate draft procedures for interim processes with the Under Secretary of Defense for Acquisition and Sustainment (OUSD(A&S)) for concurrence and finalize program business rules to support compliant JSF asset records in the Defense Property Accountability System (DPAS). The estimated completion date for completion/publication of business rules was December 31, 2024. We followed up with DOD multiple times regarding the status of the recommendation. In July 2025, our DOD point of contact told us that they are working with OUSD A&S and JPO to obtain an update and will notify us once it is received. We will continue to follow-up on the status of this recommendation.

|

| Department of Defense | The Under Secretary of Defense for Acquisition and Sustainment together with the F-35 Program Executive Officer, and in consultation with the Under Secretary of Defense (Comptroller), should finalize and implement procedures to calculate deemed cost for all JSF assets that lack documentation of historical cost data. The procedures should include the preferred deemed cost valuation methodologies and steps to prepare and retain supporting documentation for all property records created using deemed cost. (Recommendation 7) |

DOD concurred with this recommendation and stated that the F-35 Joint Program Office (JPO) has been working in coordination and consultation with the Office of the Under Secretary of Defense for Acquisition and Sustainment (OUSD(A&S)) and the Office of the Under Secretary of Defense (Comptroller) (OUSD(C)) to identify and implement procedures to calculate deemed cost for all the Joint Strike Fighter (JSF) assets that lack documentation of historical cost data. OUSD(C) staff and supporting resources are engaged directly with F-35 JPO and OUSD(A&S) to finalize and document preferred deemed cost valuation methodologies and steps to prepare and retain supporting documentation for all property records created using deemed cost. The estimated completion date for developing policies and procedures was June 30, 2024. We followed up with DOD multiple times regarding the status of the recommendation. In July 2025, our DOD point of contact told us that they are working with OUSD A&S and JPO to obtain an update and will notify us once it is received. We will continue to follow-up on the status of this recommendation.

|

| Department of Defense | The Under Secretary of Defense for Acquisition and Sustainment together with the F-35 Program Executive Officer should develop procedures to capture and record new JSF asset transactions and retain supporting documentation to support the recorded transactions after beginning balances are recorded using deemed cost. (Recommendation 8) |

DOD concurred with this recommendation and stated that with guidance and oversight from the Under Secretary of Defense for Acquisition and Sustainment (OUSD(A&S)), the F-35 Joint Program Office (JPO) will develop detailed procedures to capture and record new Joint Strike Fighter (JSF) asset transactions and retain supporting documentation as required to support the recorded transactions after beginning balances are established. The estimated completion date for developing interim procedures was September 30, 2024. We followed up with DOD multiple times regarding the status of the recommendation. In July 2025, our DOD point of contact told us that they are working with OUSD A&S and JPO to obtain an update and will notify us once it is received. We will continue to follow-up on the status of this recommendation.

|

| Department of Defense | The Under Secretary of Defense for Acquisition and Sustainment together with the F-35 Program Executive Officer should identify a complete list of JSF software applications that meet DOD's reporting criteria. (Recommendation 9) |

DOD concurred with this recommendation and stated that the F-35 Joint Program Office (JPO) will develop a complete list of Joint Strike Fighter (JSF) software applications that meet the DOD reporting criteria. This list will be updated yearly and be available on demand from the F-35 Chief Software Office. The estimated completion date to finalize or publish the list was December 31, 2024. We followed up with DOD multiple times regarding the status of the recommendation. In July 2025, our DOD point of contact told us that they are working with OUSD A&S and JPO to obtain an update and will notify us once it is received. We will continue to follow-up on the status of this recommendation.

|

| Department of Defense | The Under Secretary of Defense for Acquisition and Sustainment together with the F-35 Program Executive Officer should develop policies and procedures to record and report new JSF internal-use software development costs. (Recommendation 10) |

DOD partially-concurred with this recommendation and stated that the F-35 Joint Program Office (JPO) will develop policies and procedures to record and report new Joint Strike Fighter (JSF) internal-use software development costs. The estimated completion date for the development/publication of policies and procedures was December 31, 2024. We followed up with DOD multiple times regarding the status of the recommendation. In July 2025, our DOD point of contact told us that they are working with OUSD A&S and JPO to obtain an update and will notify us once it is received. We will continue to follow-up on the status of this recommendation.

|

| Department of Defense | The Under Secretary of Defense for Acquisition and Sustainment together with the F-35 Program Executive Officer should analyze the significance of purchase-related subsequent transportation costs on financial reporting of JSF asset balances. As needed, the office should either document the decision and rationale for not capturing these costs or develop policies and procedures for capturing and recording JSF asset purchase-related subsequent transportation costs for financial reporting. (Recommendation 11) |

DOD partially-concurred with this recommendation and stated that the Under Secretary of Defense for Acquisition and Sustainment (OUSD(A&S)) is working to establish transportation data in conjunction with efforts performed by Cost Assessment and Program Evaluation (CAPE) on program costs. The program is modifying certain process which impact subsequent transportation costs. After the new processes are in place, OUSD (A&S) and CAPE can perform an analysis on the significance of subsequent transportation costs. Once the analysis has been performed, the Joint Program Office can then address resulting decisions and rationale to support financial reporting requirements. The estimated completion date to document updated processes in place and establish contract language that provides sufficient cost information to support cost analysis requirements was June 30, 2023. The estimated completion date to perform cost analysis was September 30, 2024. We followed up with DOD multiple times regarding the status of the recommendation. In July 2025, our DOD point of contact told us that they are working with OUSD A&S and JPO to obtain an update and will notify us once it is received. We will continue to follow-up on the status of this recommendation.

|

| Department of Defense | The Under Secretary of Defense for Acquisition and Sustainment, in collaboration with the Under Secretary of Defense (Comptroller), should determine and document whether information on joint programs needed for reporting purposes is sufficiently maintained and whether a central data source and standard definition would be appropriate to help ensure consistent, complete, and accurate tracking, recording, and reporting of joint program information. (Recommendation 12) |

DOD concurred with this recommendation and stated that the Under Secretary of Defense for Acquisition and Sustainment (OUSD(A&S)) will research the needs for joint program information to determine the best source of obtaining accurate and complete information and define what a joint program is for this purpose. The estimated completion date for researching the need to establish joint program reporting was June 30, 2023 and to formalize the results of the research into policy was October 31, 2024. We followed up with DOD multiple times regarding the status of the recommendation. In July 2025, our DOD point of contact told us that they are working with OUSD A&S and OUSD (Comptroller) to obtain an update and will notify us once it is received. We will continue to follow-up on the status of this recommendation.

|