Flood Insurance: Comprehensive Reform Could Improve Solvency and Enhance Resilience

Highlights

What GAO Found

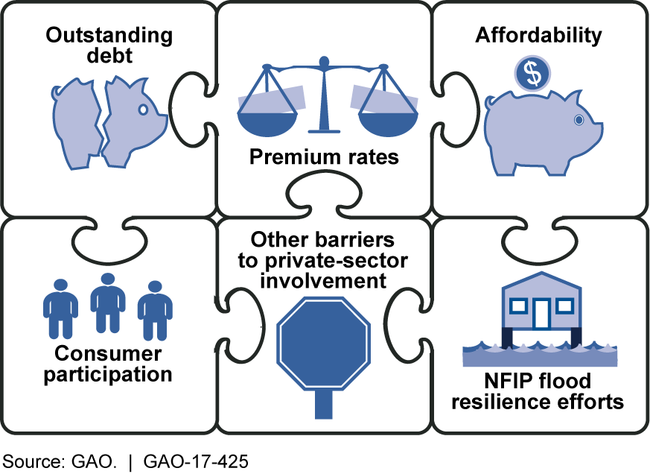

Based on discussions with stakeholders and GAO's past work, reducing federal exposure and improving resilience to flooding will require comprehensive reform of the National Flood Insurance Program (NFIP) that will need to include potential actions in six key areas (see figure below). Comprehensive reform will be essential to help balance competing programmatic goals, such as keeping flood insurance affordable while keeping the program fiscally solvent. Taking actions in isolation may create challenges for some property owners (for example, by reducing the affordability of NFIP policies) and therefore these consequences also will need to be considered. Some of the potential reform options also could be challenging to start or complete, and could face resistance, because they could create new costs for the federal government, the private sector, or property owners. Nevertheless, GAO's work suggests that taking actions on multiple fronts represents the best opportunity to help address the spectrum of challenges confronting NFIP.

Six Areas That Constitute Comprehensive Flood Insurance Reform

Through its work, GAO identified the following interrelationships and potential benefits and challenges associated with potential actions that could be taken to reform NFIP in the six areas:

- Outstanding debt. The Federal Emergency Management Agency (FEMA), which administers NFIP, owed $24.6 billion as of March 2017 to the Department of the Treasury (Treasury) for money borrowed to pay claims and other expenses, including $1.6 billion borrowed following a series of floods in 2016. FEMA is unlikely to collect enough in premiums to repay this debt. Eliminating the debt could reduce the need to raise rates to pay interest and principal on existing debt. However, additional premiums still would be needed to reduce the likelihood of future borrowing in the long term. Raising premium rates could create affordability issues for some property owners and discourage them from purchasing flood insurance, and would require other potential actions to help mitigate these challenges.

- Premium rates. NFIP premiums do not reflect the full risk of loss, which increases the federal fiscal exposure created by the program, obscures that exposure from Congress and taxpayers, contributes to policyholder misperception of flood risk (they may not fully understand the risk of flooding), and discourages private insurers from selling flood insurance (they cannot compete on rates). Eliminating rate subsidies by requiring all rates to reflect the full risk of loss would address an underlying cause of NFIP's debt and minimize federal fiscal exposure. It also would improve policyholder understanding of flood risk and encourage private-sector involvement. However, raising rates makes policies less affordable and could reduce consumer participation. The decreases in affordability could be offset by other actions such as providing means-based assistance.

- Affordability. Addressing the affordability issues that some consumers currently face, or might face if premium rates were raised, could help ensure more consumers purchase insurance to protect themselves from flood losses. GAO previously recommended that any affordability assistance should be funded with a federal appropriation (rather than through discounted premiums) and should be means-tested. Means-testing the assistance could help control potential costs to the federal government, and funding with an appropriation would increase transparency of the federal fiscal exposure to Congress. Many industry and nonindustry stakeholders with whom GAO spoke said affordability assistance should focus on helping to pay for mitigation—such as elevating buildings—because mitigation permanently reduces flood risk (thus reducing premium rates). Mitigation efforts can have high up-front costs, and may not be feasible in all cases, but many stakeholders suggested that federal loans could be used to spread consumer costs over time.

- Consumer participation. According to many industry and nonindustry stakeholders with whom GAO spoke, some consumers might not purchase flood insurance because they misperceive their flood risk. For example, consumers located outside of the highest-risk areas, who are not required to purchase flood insurance, may mistakenly perceive they are not at risk of flood loss. Consumers also may choose not to purchase flood insurance because they overestimate the adequacy of federal assistance they would expect to receive after a disaster. Expanding the mandatory purchase requirement beyond properties in the highest-risk areas is one option for encouraging consumer participation in flood insurance. However, doing so could face public resistance and create affordability challenges for some, highlighting the importance of an accompanying affordability assistance program. Increasing consumer participation could help ensure more consumers would be better protected from the financial risk of flooding.

- Other barriers to private-sector involvement. Industry and nonindustry stakeholders with whom GAO spoke cited regulatory uncertainty and lack of data as barriers to their ability to sell flood insurance, in addition to the less than full-risk rates charged by FEMA. For example, some industry and nonindustry stakeholders told GAO that while lenders must enforce requirements that certain mortgages have flood insurance, some lenders are uncertain whether private policies meet the requirements. Clarifying the types of policies and coverage that would do so could reduce this uncertainty and encourage the use of private flood insurance. In addition, some stakeholders said that access to NFIP claims data by the insurance industry could allow private insurers to better estimate losses and price policies. FEMA officials said they would need to address privacy concerns to provide such information but have been exploring ways to facilitate more data sharing.

- NFIP flood resilience efforts. Some industry and nonindustry stakeholders told GAO that greater involvement by private insurers could reduce funding available for some NFIP flood resilience efforts (mitigation, mapping, and community participation). For example, some of these stakeholders said that as the number of NFIP policies decreased, the policy fees FEMA used to help fund mitigation and flood mapping activities also would decrease. Potential actions to offset such a decrease could include appropriating funds for these activities or adding a fee to private policies. This would allow NFIP flood resilience efforts to continue at their current levels as private-sector involvement increased.

Why GAO Did This Study

Congress created NFIP to reduce the escalating costs of federal disaster assistance for flood damage, but also prioritized keeping flood insurance affordable, which transferred the financial burden of flood risk from property owners to the federal government. In many cases, premium rates have not reflected the full risk of loss, so NFIP has not had sufficient funds to pay claims. As of March 2017, NFIP owed $24.6 billion to Treasury. NFIP's current authorization expires in September 2017.

In this report, GAO focuses on potential actions that can help reduce federal fiscal exposure and improve resilience to flood risk. GAO reviewed laws, GAO reports, and other studies. GAO interviewed officials from FEMA and other agencies. GAO also solicited input from industry stakeholders (including insurers, reinsurers, and actuaries) and nonindustry stakeholders (including academics, consumer groups, and real estate and environmental associations) through interviews, a nongeneralizable questionnaire, and four roundtable discussions.

Recommendations

To improve NFIP solvency and enhance national resilience to floods, Congress should consider comprehensive reform covering six areas: (1) outstanding debt, (2) premium rates, (3) affordability, (4) consumer participation, (5) barriers to private-sector involvement, and (6) NFIP flood resilience efforts.

Matter for Congressional Consideration

| Matter | Status | Comments |

|---|---|---|

| As Congress considers reauthorizing NFIP, it should consider comprehensive reform to improve the program's solvency and enhance the nation's resilience to flood risk, which could include actions in six areas: (1) addressing the current debt, (2) removing existing legislative barriers to FEMA's revising premium rates to reflect the full risk of loss, (3) addressing affordability, (4) increasing consumer participation, (5) removing barriers to private-sector involvement, and (6) protecting NFIP flood resilience efforts. In implementing these reforms, Congress should consider the sequence of the actions and their interaction with each other. | As of February 2026, Congress has not enacted legislation in response to this matter. |