Tennessee Valley Authority: Actions Needed to Better Communicate Debt Reduction Plans and Address Billions in Unfunded Pension Liabilities

Fast Facts

The Tennessee Valley Authority, the nation's largest public power provider, provides electricity to more than 9 million customers. It raises billions in revenue but also issues bonds to finance its large capital investments (though it is subject to a $30-billion debt limit).

The TVA plans to reduce its debt by about $4 billion by 2023 by increasing rates and reducing expenses; it also plans to eliminate its unfunded pension liabilities.

However, we found that its debt reduction goals and plans haven't been reported as required. We recommended that it do so, and that it take steps to ensure that its pension plan is fully funded.

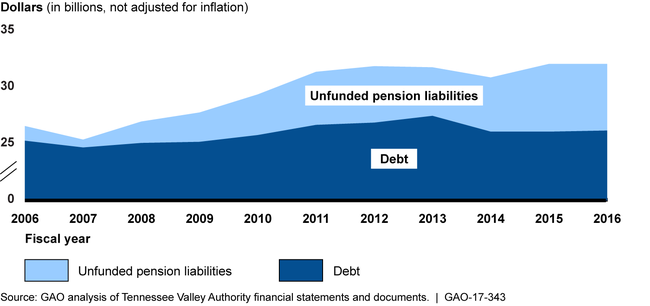

Tennessee Valley Authority's Debt and Unfunded Pension Liabilities, Fiscal Years 2006-2016

Figure illustrates TVA's debt and growing unfunded pension liabilities.

Highlights

What GAO Found

To meet its goal to reduce debt by about $4 billion—from about $26 billion in fiscal year 2016 to about $22 billion by fiscal year 2023—the Tennessee Valley Authority (TVA) plans to increase rates, limit the growth of operating expenses, and reduce capital expenditures. For example, TVA increased rates each fiscal year from 2014 through 2017 and was able to reduce operating and maintenance costs by about 18 percent from fiscal year 2013 to 2016. TVA's plans depend on assumptions that future capital projects will be completed on time and within budget, but TVA's estimated capital costs may be optimistic and could increase.

TVA's debt reduction plans and performance information are not reported in a manner consistent with the GPRA Modernization Act of 2010. Specifically, TVA identifies managing its debt and its unfunded pension liabilities as major management challenges but has not reported required performance information in its performance plans or reports on these challenges, thereby reducing transparency and raising questions about how it will meet its goal. As of September 30, 2016, TVA‘s pension plan was about 54 percent funded (plan assets totaled about $7.1 billion and liabilities $13.1 billion). While TVA's debt has remained relatively flat, its unfunded pension liabilities have steadily increased over the past 10 years, as shown below.

Tennessee Valley Authority's Debt and Unfunded Pension Liabilities, Fiscal Years 2006 through 2016

Several factors could affect TVA's ability to meet its debt reduction goal, including regulatory pressures, changes in demand for electricity, technological innovations, or unforeseen events. Also, TVA aims to eliminate its unfunded pension liabilities within 20 years, according to TVA officials. However, factors such as market conditions could affect TVA's progress, and no mechanism is in place to ensure it fully funds the pension liabilities if, for example, plan assets do not achieve expected returns. The TVA retirement system rules that determine TVA's required annual pension contributions do not adjust TVA's contributions to ensure full funding and TVA does not plan to contribute more than the rules require. Without a mechanism that ensures TVA's contributions will adequately adjust for actual plan experience, unfunded liabilities could remain and future ratepayers may have to fund the pension plan even further to pay for services provided to prior generations of ratepayers.

Why GAO Did This Study

TVA, the nation's largest public power provider, is a federal electric utility with revenues of about $10.6 billion in fiscal year 2016. TVA's mission is to provide affordable electricity, manage river systems, and promote economic development. TVA provides electricity to more than 9 million customers in the southeastern United States. TVA must finance its assets with debt and operating revenues. TVA primarily finances large capital investments by issuing bonds but is subject to a statutorily imposed $30 billion debt limit. In fiscal year 2014, TVA established a debt reduction goal.

GAO was asked to review TVA's plans for debt reduction. This report examines (1) TVA's debt reduction goal, plans for meeting its goal, and key assumptions; (2) the extent to which TVA reports required performance information; and (3) factors that have been reported that could affect TVA's ability to meet its goal. GAO analyzed TVA financial data and documents and interviewed TVA and federal officials and representatives of stakeholder and industry groups.

Recommendations

GAO recommends that TVA (1) better communicate its plans and goals for debt reduction and reducing unfunded pension liabilities in its annual performance plan and report and (2) take steps to have its retirement system adopt funding rules designed to ensure the pension plan's full funding. TVA agreed with the first recommendation and neither agreed nor disagreed with the second. GAO believes that action is needed as discussed in the report.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Tennessee Valley Authority | The Board of Directors should ensure that TVA better document and communicate its goals to reduce its debt and unfunded pension liabilities in its performance plans and reports, including detailed strategies for achieving these goals. |

TVA concurred with this recommendation and said it would implement it. TVA has taken steps to better document and communicate its goals to reduce debt and unfunded pension liabilities and provide information on its plans for achieving these goals. Specifically, in TVA's FY 2017 and FY 2018 annual performance reports, TVA reported its goals and plans for reducing debt to $21.8 billion by FY 2023 and fully funding its defined benefit plan.

|

| Tennessee Valley Authority | The Board of Directors should ensure that TVA propose, and work with the TVA Retirement System board to adopt, funding rules designed to ensure the plan's full funding. |

In their initial response to our report, TVA neither agreed nor disagreed with this recommendation. In response to our report, TVA has taken some steps to improve the plan's funding status. For example, in fiscal year 2017, TVA made a one-time pension contribution of $500 million to the TVA Retirement System (TVARS) in addition to its $300 million required annual contribution. Also, in FY 2021, TVA and TVARS adopted a new asset allocation policy and de-risking strategy that aims to enhance stability in the plan's asset value and reduce the funded status volatility. TVA's one-time contribution and investment returns have improved the funding status of the TVARS plan but the TVARS Rules do not adjust TVA's required contributions to ensure pension liabilities will be fully funded. To fully implement this recommendation, the Rules need a mechanism that adjusts TVA's contributions to ensure adequate funding regardless of future plan experience. According to TVA's financial statement, as of September 30, 2024, TVA's qualified pension plan had assets of approximately $8.7 billion compared to liabilities of approximately $11.0 billion.

|