DOD Financial Management: Additional Actions Needed to Achieve a Clean Audit Opinion on DOD’s Financial Statements

Fast Facts

DOD has been working to improve its long-standing financial management problems and achieve its goal of a "clean" audit opinion on its financial statements. A clean opinion is when auditors find that the statements are presented fairly and consistent with accounting principles.

DOD has taken steps, such as developing corrective actions and roadmaps, to get to a clean audit opinion. But we found DOD's plans didn't have enough information, including detailed procedures for addressing known problems. We recommended that DOD develop a comprehensive plan to address these issues.

DOD's financial management has been on our High Risk List since 1995.

Highlights

What GAO Found

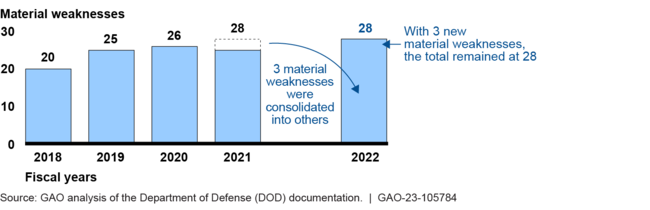

The Department of Defense's (DOD) financial statement audits for fiscal year 2022 and prior years have resulted in disclaimers of opinion—meaning that auditors were unable to obtain sufficient, appropriate evidence to provide a basis for an audit opinion. Fiscal year 2018 was the first year that DOD underwent its full-scope consolidated financial statement audit. For that and each subsequent fiscal year, auditors identified material weaknesses, which are serious deficiencies that affect DOD's financial reporting (see figure). Auditors also issued thousands of notices of findings and recommendations (NFR).

Department of Defense Material Weaknesses Identified by Auditors

The financial statement audit has value far beyond the audit opinion. It can help to identify vulnerabilities and ways to improve operations. DOD audits have resulted in short- and long-term benefits. The audits helped identify assets that DOD did not know existed. For example, in fiscal year 2020, Navy identified and added nearly $2.4 billion of unrecorded inventory, operating materials and supplies, and general equipment. These items were subsequently used to fill over 12,000 requisitions, which otherwise would have cost $50 million in material.

DOD has taken steps to achieve an unmodified (clean) audit opinion—when the auditor finds that financial statements are presented fairly in accordance with U.S. generally accepted accounting principles. These steps include developing audit priority areas, a financial management strategy, corrective action plans, and audit roadmaps. However, GAO found that these DOD plans lack details that are important to achieving a clean audit opinion. For example, DOD's audit roadmaps do not have interim milestone activities and dates to show the steps for reaching overall target remediation goals. Also, DOD's financial management strategy focuses on high-level DOD financial management priorities and is not specific to achieving a clean opinion. A comprehensive plan with a clear DOD-wide vision for how to achieve a clean audit opinion, with detailed procedures for addressing material weaknesses, would help DOD to reach this milestone.

GAO also found that DOD has consistently missed target remediation dates provided in its DOD-wide roadmap. DOD needs to take steps to improve audit roadmaps—including considering dependencies identified by components, analyzing the feasibility of estimated target remediation dates, and reassessing actions as needed. Without these steps, DOD and components will be at increased risk of continuing to miss and extend target remediation dates, further hindering its ability to achieve a clean audit opinion.

Why GAO Did This Study

DOD is responsible for about half of the federal government's discretionary spending. However, DOD remains the only major federal agency that has never been able to receive a clean audit opinion on its financial statements. Since 1995, GAO has designated DOD financial management as high risk because of pervasive deficiencies in its financial management systems, business processes, internal controls, and financial reporting.

House Report 117-88 includes a provision for GAO to review DOD's efforts to achieve a clean audit opinion by 2027. This report examines the (1) status of DOD's efforts to achieve a clean opinion, and benefits of the audits, and (2) extent to which DOD developed plans to address audit findings and achieve a clean opinion.

GAO reviewed relevant DOD and DOD Office of Inspector General reports, as well as memorandums and status reports; interviewed officials; and analyzed NFR data related to DOD's material weaknesses. GAO also assessed DOD and military departments' corrective action plans and roadmaps.

Recommendations

GAO is making five recommendations, including for DOD to develop and document a comprehensive plan to achieve a clean audit opinion and to consider dependencies and analyze the feasibility of remediation dates in roadmaps. DOD concurred with one recommendation, partially concurred with three, and did not concur with one. GAO maintains that all of the recommendations are warranted.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Department of Defense | The Secretary of Defense should ensure that the Under Secretary of Defense (Comptroller), in collaboration with the Secretaries of Navy, Air Force, and Army, develops and documents a DOD-wide comprehensive plan to coordinate its efforts to achieve a clean audit opinion. The plan should include a clear statement of the DOD-wide vision for how to achieve a clean audit opinion and complete, detailed procedures for addressing material weaknesses, with interim milestone activities and dates. (Recommendation 1) |

In its comments on our draft report, DOD did not concur with this recommendation. DOD stated that it has already established a clear plan and vision toward DOD's objective of improving its financial management process and procedures. However, it is not clear as to what DOD's plan and vision for achieving a clean audit opinion is and whether it is documented or comprehensive, as it was not provided to us. As of September 2025, DOD has not provided updated information. We will continue to monitor DOD efforts to address this recommendation.

|

| Department of Defense | The Under Secretary of Defense (Comptroller) should document the consideration of dependencies identified in component-level roadmaps when developing its DOD-wide roadmap. (Recommendation 2) |

In its comments on our draft report, DOD partially concurred with this recommendation. DOD stated that components are required to identify the dependencies in component-level roadmaps in support of the remediation dates for each identified component-level material weakness. In addition, DOD stated that considerations to timeline adjustments are made at the components' discretion. However, the consideration of dependencies that would need to be resolved before material weaknesses could be remediated is not documented. As of September 2025, DOD has not provided updated information. We will continue to monitor DOD efforts to address this recommendation.

|

| Department of Defense | The Under Secretary of Defense (Comptroller) should develop monitoring procedures to reasonably assure consistent and accurate support for tracking, recording, and reporting of target remediation dates presented in all component-level roadmaps when developing its DOD-wide roadmap. (Recommendation 3) |

In its comments on our draft report, DOD partially concurred with this recommendation. DOD stated that it has established the oversight and monitoring function for component-level target remediation dates through the Audit Roadmap Dashboard. DOD also stated that the Financial Improvement and Audit Remediation Committee and Governance Board, Property/IT Functional Councils, and Deputy's Management Action Group meetings are leveraged to monitor and address components' efforts to remediate identified audit deficiencies. Although DOD relies on these meetings and status updates discussed in them to broadly monitor remediation efforts, the meetings do not address our recommendation to develop monitoring procedures for remediation dates. As of September 2025, DOD has not provided updated information. We will continue to monitor DOD efforts to address this recommendation.

|

| Department of Defense | The Under Secretary of Defense (Comptroller) should develop and implement procedures to analyze the feasibility of estimated target remediation dates included in the DOD-wide roadmap. Such procedures should include steps to reassess actions and adjust plans if the analysis shows that the estimated dates cannot be met. (Recommendation 4) |

In its comments on our draft report, DOD partially concurred with this recommendation. DOD stated that throughout the audit fiscal year, it discusses and develops DOD-wide remediation efforts and plans to analyze the feasibility of estimated target remediation dates documented in the DOD-wide audit roadmaps. DOD also stated that the Under Secretary of Defense (Comptroller) will implement additional procedures to analyze the feasibility of the estimated target remediation dates included in the DOD-wide roadmap. As of September 2025, DOD has not provided updated information. We will continue to monitor DOD efforts to address this recommendation.

|

| Department of Defense | The Under Secretary of Defense (Comptroller) should issue additional guidance to components, including the military departments, for developing appropriate and supportable timelines in component-level roadmaps. (Recommendation 5) |

In its comments on our draft report, DOD concurred with this recommendation. DOD stated that the Under Secretary of Defense (Comptroller) will issue guidance to specifically instruct the component-level audit roadmaps to include appropriate and supportable timelines. As of September 2025, DOD has not provided updated information. We will continue to monitor DOD efforts to address this recommendation.

|