A Tax Reform State of Mind

- What should we tax? Do we continue with the current system, which taxes the income that individuals and companies earn, or move to something like a national sales tax (which just taxes income when it’s spent)?

- Who should pay and how much? Should wealthier taxpayers pay more than those that are less well off, or should taxpayers pay based on the benefits they receive?

- How much tax revenue should be collected? Taxes fund government services, and reforming the tax code could raise or lower taxes—creating a surplus or deficit of revenue collected. If the government collects less revenue than it spends, it will have to borrow the difference and pay interest on that amount.

- How will taxes affect the decisions taxpayers make? Will taxpayers save, work, or consume more or less because of the tax?

- Finally, will taxpayers be able to understand and comply with the tax? Will there be more or fewer taxpayers? And, will the IRS be able to administer the tax?

- What tax rate should corporations pay? The United States taxes the income of corporations using a graduated corporate income tax rate. These tax rates range from 15 percent for corporations that make less than $50,000 to 35 percent for those that make more than about $18 million. However, when you account for the various exemptions, tax credits, and other tax benefits large corporations receive, they (on average) paid a rate of about 25 percent of their pretax net income in taxes from 2008 to 2012.

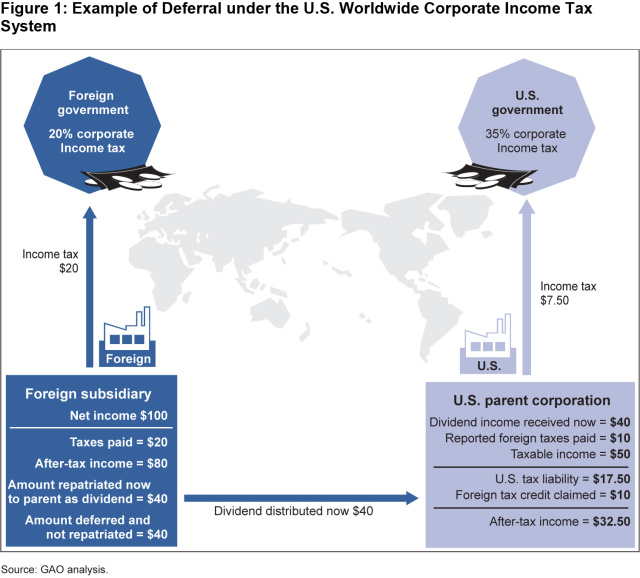

- How should the income U.S. corporations earn abroad be taxed (if at all)? The current system taxes all income made by U.S. corporations and their subsidiaries, including income they earn abroad. However, income earned abroad by U.S.-owned subsidiaries is only taxed when it’s brought back to the United States—generally when a foreign subsidiary sends back dividends to the U.S. corporation that owns it. This can distort corporate investment and location decisions—for example, a U.S. corporation may keep money abroad because it is in a country with low taxes instead of putting that money into more productive use in the U.S. (e.g., investing in research).

- Questions on the content of this post? Contact James R. McTigue, Jr. at mctiguej@gao.gov or Jessica K. Lucas-Judy at lucasjudyj@gao.gov.

- Comments on GAO’s WatchBlog? Contact blog@gao.gov

GAO's mission is to provide Congress with fact-based, nonpartisan information that can help improve federal government performance and ensure accountability for the benefit of the American people. GAO launched its WatchBlog in January, 2014, as part of its continuing effort to reach its audiences—Congress and the American people—where they are currently looking for information.

The blog format allows GAO to provide a little more context about its work than it can offer on its other social media platforms. Posts will tie GAO work to current events and the news; show how GAO’s work is affecting agencies or legislation; highlight reports, testimonies, and issue areas where GAO does work; and provide information about GAO itself, among other things.

Please send any feedback on GAO's WatchBlog to blog@gao.gov.