Regulatory Guidance Processes: Treasury and OMB Need to Reevaluate Long-standing Exemptions of Tax Regulations and Guidance

Highlights

What GAO Found

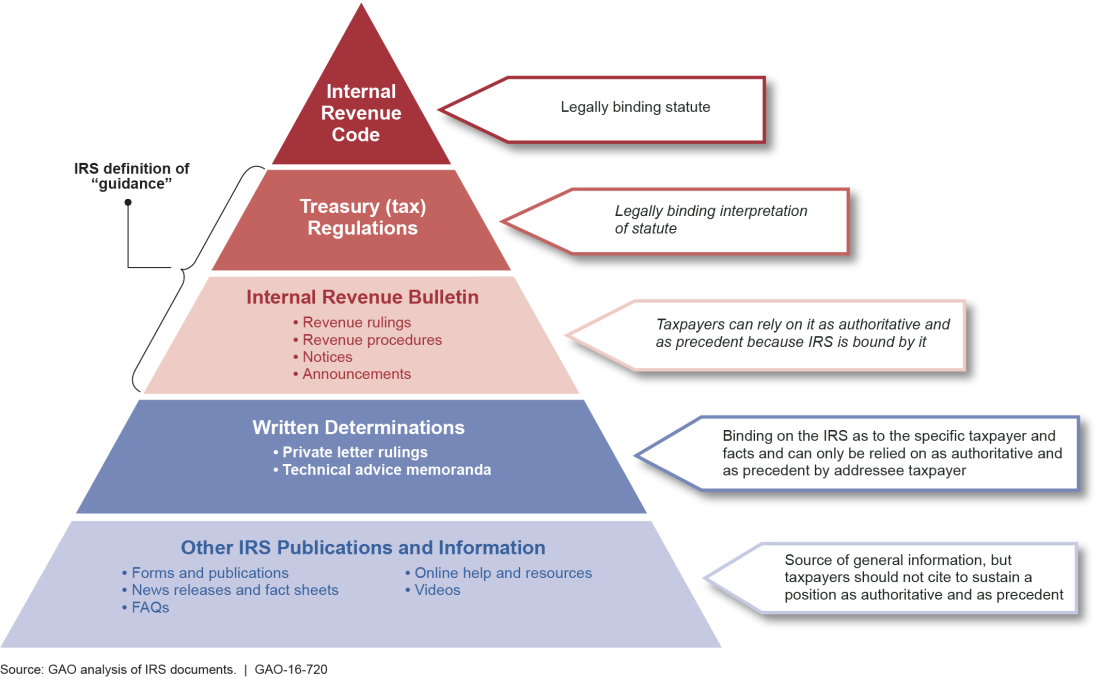

The Internal Revenue Service (IRS) uses a variety of documents to communicate its interpretation of tax laws to the public, but only considers Internal Revenue Bulletin (IRB) guidance to be authoritative. IRS information published outside of the IRB can help taxpayers understand tax laws and make informed decisions, but does not always include information clarifying the limitations of its use. IRS has detailed procedures for identifying, prioritizing, and issuing new guidance. However, it lacks procedures for documenting the decision about what type of guidance to issue.

Hierarchy of Authority for IRS Guidance and Other Information Sources

In a review of tax guidance, GAO found few instances in which the Office of Management and Budget (OMB) determined that a tax regulation was likely to have significant economic effects and would thus be subject to additional analysis. OMB's significance determinations largely result from initial assessments by the Department of Treasury (Treasury) and IRS that many administrative law or executive order requirements do not apply to most tax regulations and other guidance. Some tax regulations and other guidance are also exempt from further analysis and review under a 1983 agreement between OMB and Treasury, which was reaffirmed in 1993. This agreement has not been revisited in more than 20 years, and it is unclear whether this agreement is still relevant.

GAO also reviewed eight case files of non-regulatory IRS guidance documents published in 2015 and found that IRS did not consistently document required steps during key phases of the issuance process. Although these eight case files are non-generalizable, documenting key decisions may help IRS evaluate the risk of challenges to IRS assessments about whether tax guidance is significant enough to warrant additional OMB and congressional review.

Why GAO Did This Study

The public relies on IRS guidance to understand complex tax laws and meet their responsibilities. GAO was asked to examine IRS guidance and rulemaking processes. This report reviews (1) how IRS communicates its interpretation of tax laws to the public and decides what type of guidance to issue; (2) what relevant authorities apply and what policies and procedures IRS uses when issuing guidance; and (3) to what extent selected IRS guidance products followed relevant authorities. GAO reviewed IRS policies and procedures for issuing guidance, conducted literature reviews, analyzed eight non-generalizable case files for compliance with relevant authorities, and interviewed agency officials and other subject matter experts.

Recommendations

GAO is making six recommendations, including that IRS communicate more clearly the limitations of information not published in the IRB, and that IRS develop procedures to better document the type of guidance it plans to issue and the key decisions made during the evaluations. GAO also recommends that Treasury and OMB reevaluate their long-standing agreement to exempt some tax guidance and regulations from OMB oversight. IRS and Treasury agreed with all of GAO's recommendations, and OMB neither agreed nor disagreed.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Internal Revenue Service | The Commissioner of Internal Revenue should communicate more clearly the limitations of information not published in the IRB to taxpayers. Such action could include adding clarifying language to some pieces of information not published in the IRB, like FAQs, and amending policies and procedures, such as the Internal Revenue Manual (IRM), to clarify when IRS information should contain a statement regarding its legal authority and whether the item can be used or cited as precedent. |

Based on our report, in May 2017, IRS issued guidance to its examiners reminding them that FAQs and other items posted on IRS.gov, but not published in the Internal Revenue Bulletin, are not legal authority. Further, in January 2018, IRS amended the Internal Revenue Manual section 4.10.7 to caution revenue examiners that some FAQs appearing on IRS's website, but not published in the Internal Revenue Bulletin, are not legal authority and should not be used to sustain a position.

|

| Internal Revenue Service | The Commissioner of Internal Revenue should amend current policies and procedures for drafting guidance to include factors to consider when deciding what type of guidance to issue and procedures for documenting those decisions internally. |

Based on our report, in April 2017, IRS revised language in the Chief Counsel Directives Manual (CCDM) to address this recommendation. Specifically, IRS revised CCDM section 32.1.1.2 to provide factors to consider when determining the appropriate form of guidance.

|

| Internal Revenue Service | The Commissioner of Internal Revenue should develop policies and procedures to help guidance-drafting teams assess whether non-regulatory guidance should be considered a rule for purposes of the Congressional Review Act (CRA) and in turn major, and document those assessments internally. |

Based on our report, in April 2017, IRS revised language in the Chief Counsel Directives Manual (CCDM) to address this recommendation. Specifically, IRS revised CCDM section 32.2.8.2 to clarify procedures for documenting determinations of whether non-regulatory guidance is a rule under CRA, and ensuring congressional review.

|

| Internal Revenue Service | The Commissioner of Internal Revenue should take action to ensure that required steps are consistently documented during key phases of the non-regulatory guidance process, as defined in the Chief Counsel Directives Manual. |

In April 2017, IRS reviewed its current information system for managing the drafting of tax regulations and other guidance, and determined that it served as an effective control. Based on our report, IRS also sent communications to its guidance drafting offices reiterating the importance of following procedures especially the required use of a key tracking document to control the process of drafting and clearing guidance.

|

| Department of the Treasury |

Priority Rec.

The Director of the Office of Management and Budget and the Secretary of the Treasury should examine the relevance of the long-standing agreement that exempts certain IRS regulations from executive order requirements and Office of Information and Regulatory Affairs (OIRA) oversight; and if relevant, make publicly available any reaffirmation of the agreement and the reasons for it. |

Treasury agreed with this recommendation. In April 2018, the Treasury general counsel and the OIRA administrator signed a new Memorandum of Agreement that supersedes the 1983 memorandum and sets forth new terms under which OIRA will review tax regulatory actions.

|

| Office of Management and Budget | The Director of the Office of Management and Budget and the Secretary of the Treasury should examine the relevance of the long-standing agreement that exempts certain IRS regulations from executive order requirements and Office of Information and Regulatory Affairs (OIRA) oversight; and if relevant, make publicly available any reaffirmation of the agreement and the reasons for it. |

In April 2018, the Treasury general counsel and the OIRA administrator signed a new Memorandum of Agreement that supersedes the 1983 memorandum and sets forth new terms under which OIRA will review tax regulatory actions.

|

| Department of the Treasury | The Director of Office of Management and Budget and the Secretary of the Treasury should develop a process to ensure that OIRA has the information necessary to determine whether IRS rules are major under CRA and significant under E.O.12866. Consideration should be given on ways to solicit public comments on the potential effects of proposed regulations and non-regulatory guidance, including measures of economic impacts, and on how to document internally the consideration of significant comments by both IRS and OIRA. |

Based on our report, in April 2018, the Treasury general counsel and the OIRA administrator signed a new Memorandum of Agreement that addresses the review of tax regulations under Executive Order 12866. The memorandum includes the following language: "To facilitate the determinations set forth in paragraph 1 (which include determination of economic significance), Treasury will submit to OIRA a quarterly notice of planned tax regulatory actions that describe each action; and articulates the basis for determining whether the regulatory action is covered by the Memorandum of Agreement." Providing greater information to OIRA will help bring greater scrutiny to the potentially major budgetary and economic effects of tax regulations, which we have been recommending in our body of work on tax expenditures.

|

| Office of Management and Budget | The Director of Office of Management and Budget and the Secretary of the Treasury should develop a process to ensure that OIRA has the information necessary to determine whether IRS rules are major under CRA and significant under E.O.12866. Consideration should be given on ways to solicit public comments on the potential effects of proposed regulations and non-regulatory guidance, including measures of economic impacts, and on how to document internally the consideration of significant comments by both IRS and OIRA. |

Based on our report, in April 2018, the Treasury general counsel and the OIRA administrator signed a new Memorandum of Agreement that addresses the review of tax regulations under Executive Order 12866. The memorandum includes the following language: "To facilitate the determinations set forth in paragraph 1 (which include determination of economic significance), Treasury will submit to OIRA a quarterly notice of planned tax regulatory actions that describe each action; and articulates the basis for determining whether the regulatory action is covered by the Memorandum of Agreement." Providing greater information to OIRA will help bring greater scrutiny to the potentially major budgetary and economic effects of tax regulations, which we have been recommending in our body of work on tax expenditures.

|