Pension Advance Transactions: Questionable Business Practices and the Federal Response

Highlights

What GAO Found

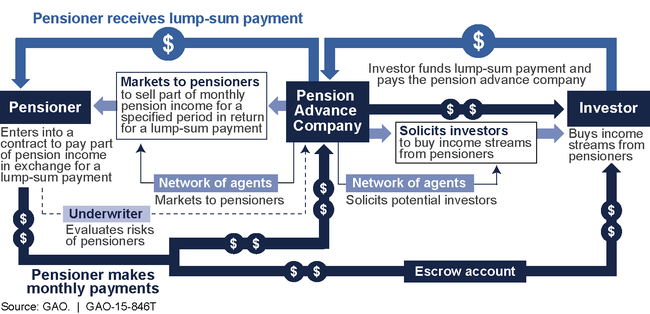

In a June 2014 report, GAO identified at least 38 companies that offered individuals lump-sum payments or “advances” in exchange for receiving part or all of their pension payment streams. The 38 companies used multistep pension advance processes that included various other parties. At least 21 of the 38 companies were affiliated with each other in ways that were not apparent to consumers. Some companies targeted financially vulnerable consumers with poor or bad credit nationwide.

Parties Involved in the Multistep Pension Advance Processes That GAO Reviewed

GAO undercover investigators received offers from 6 out of 19 pension advance companies. These offers did not compare favorably with other financial products or offerings, such as loans and lump-sum options through pension plans. For example, the effective interest rates on pension advances offered to GAO's investigators typically ranged from approximately 27 percent to 46 percent, which were at times close to two to three times higher than the legal limits set by the related states on the interest rates assessed for various types of personal credit.

GAO identified questionable elements of pension advance transactions, including lack of disclosure of some rates or fees, and certain unfavorable terms of agreements. GAO recommended that the Bureau of Consumer Financial Protection (CFPB) and Federal Trade Commission (FTC)—the two agencies with oversight responsibility over certain acts and practices that may harm consumers—provide consumer education about these products, and that CFPB take appropriate action regarding identified questionable practices.

Since the time of GAO's review, CFPB has investigated pension advance companies that GAO referred to the agency and disseminated additional consumer-education materials on pension advances. Similarly, FTC posted consumer education on pension advances on its website, and FTC officials report that they have reviewed consumer complaints related to pension advances, pension advance advertising, and the pension advance industry overall. CFPB's and FTC's actions are a positive step toward strengthening federal oversight or enforcement of pension advance products.

Why GAO Did This Study

Recent questions have been raised about companies attempting to take advantage of retirees using pension advances. In June 2014, GAO issued a report on pension advances. The report (1) described the number and characteristics of pension advance companies and marketing practices; (2) evaluated how pension advance terms compare with those of other products; and (3) evaluated the extent to which there is federal oversight.

This testimony summarizes GAO's June 2014 report (GAO-14-420) and actions taken by CFPB and FTC in response to GAO's recommendations. In June 2014, GAO identified 38 pension advance companies and related marketing practices. GAO conducted a detailed nongeneralizable assessment of 19 of these companies. GAO used undercover investigative phone calls to identify additional marketing practices and obtain pension advance offers. This information was compared with the terms of other financial products, such as personal loans. GAO also examined the role of selected federal agencies with oversight of consumer protection and pension issues.

Recommendations

In its June 2014 report, GAO recommended that CFPB and FTC review the pension advance practices identified in that report and exercise oversight or enforcement as appropriate. GAO also recommended that CFPB coordinate with relevant agencies to increase consumer education about pension advances. CFPB and FTC agreed with and have taken actions to address GAO's recommendations.