Troubled Asset Relief Program: Treasury Could More Consistently Analyze Potential Benefits and Costs of Housing Program Changes

Highlights

What GAO Found

Between February 2009 and May 2015, the U.S. Department of the Treasury (Treasury) disbursed approximately $16.3 billion of the $37.5 billion in Troubled Asset Relief Program (TARP) funds allocated to support housing programs. The number of new borrowers with permanent modifications added to the Home Affordable Modification Program (HAMP), the key component of these programs, began to decline in late 2013 but has stabilized at between 9,000 and 15,000 additions per month. Activity under HAMP Tier 1, the original modification for qualified borrowers seeking to reduce their mortgage payments to affordable levels (rates periodically reset), has gradually declined. HAMP Tier 2, a broader fixed rate modification announced in 2012, has gradually grown to account for the majority of new entrants. Since October 2014, Treasury has expanded incentives in order to draw new entrants into the programs and further assist existing participants.

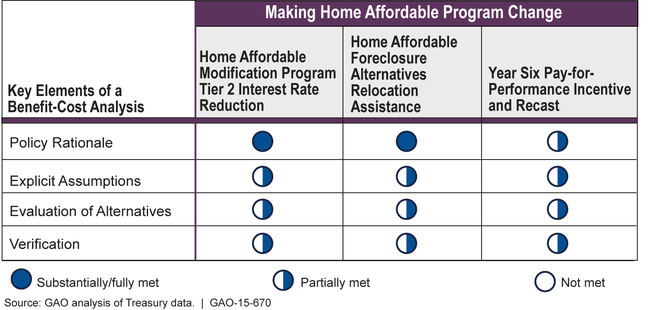

In making program changes, Treasury took steps to assess their benefits and costs but did not fully meet all of the key elements of federal benefit-cost analysis guidance, and thus has limited assurance that the additional expenditures are an effective and efficient use of taxpayer dollars (see figure below). For example, it is unclear whether the recent changes, such as extending performance incentives to borrowers in the sixth year of their HAMP modification (estimated to cost $4-6 billion), will reduce redefaults. Treasury officials told GAO that borrower surveys confirmed that borrowers responded to performance incentives. But Treasury does not have the estimates needed to fully assess the effectiveness of this or other recent changes. Treasury officials said that program benefits and costs depended on unknown factors and macroeconomic trends and that program benefits were difficult to quantify. Office of Management and Budget guidance and GAO's past work stress that analyzing benefits and costs can help decision makers choose among alternatives. Without full and comprehensive analyses, Treasury will be challenged to determine whether program changes are actually achieving desired goals and are an efficient use of taxpayer dollars.

Extent Treasury Met the Four Key Elements of OMB Circular A-94's Benefit-Cost Analysis for Three Recent Program Changes

Why GAO Did This Study

Treasury has allocated $37.5 billion in TARP funds to help struggling homeowners avoid potential foreclosure since 2009. The Emergency Economic Stabilization Act of 2008 includes a provision for GAO to report every 60 days on TARP activities. This 60-day report examines (1) the status of TARP-funded housing programs and (2) the extent to which Treasury's analytic framework for considering recent program changes was consistent with federal guidance and best practices. To do this work, GAO analyzed borrower participation levels, reviewed program documentation, and interviewed Treasury officials.

Recommendations

To bring greater rigor and efficiency to decisions about the use of federal funds, GAO recommends that Treasury develop and implement policies and procedures that establish a standard process to better ensure that TARP-funded housing program changes are based on benefit-cost analyses that meet key elements. Treasury agreed to consider applying GAO's recommendation going forward.

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Department of the Treasury | To bring greater rigor and efficiency to decisions about the use of federal funds allocated for TARP housing programs, the Secretary of the Treasury should develop and implement policies and procedures that establish a standard process to better ensure that TARP-funded housing program changes are based on analyses that comprehensively and consistently meet the key elements of benefit-cost analysis. |

Congress established December 31, 2016, as the termination date for the TARP-funded Making Home Affordable (MHA) program, with an exemption for Home Affordable Modification Program loan modification applications made before that date. In its comment letter on the draft report and in subsequent correspondence, Treasury agreed that it is important to assess the benefits and costs of proposed program improvements, and that it would continue to do so. Treasury has not subsequently made any significant policy changes to the MHA programs prior to the application deadline of December 30, 2016.

|