Troubled Asset Relief Program: Status of the Wind Down of the Capital Purchase Program

Highlights

What GAO Found

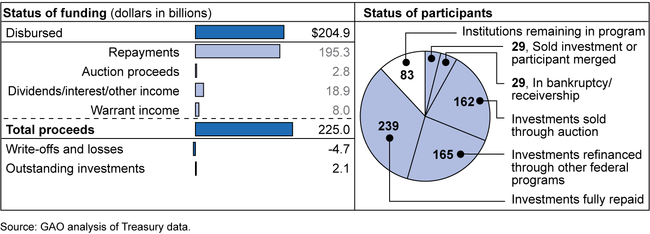

The Department of Treasury (Treasury) continues to make progress in winding down the Capital Purchase Program (CPP). As of January 31, 2014, Treasury's data showed that 624 of the original 707 institutions, or about 88 percent, had exited CPP. Treasury had received about $225 billion from its CPP investments, exceeding the approximately $205 billion it had disbursed. Most institutions exited by repurchasing their preferred shares in full or by refinancing their investments through other federal programs. Treasury also continues to sell its investments in the institutions through auctions; a strategy first implemented in March 2012 to expedite the exit of a number of CPP participants. As of January 31, 2014, Treasury has sold all or part of its CPP investment in 162 institutions through auctions, receiving a total of about 80 percent of the principal amount. A relatively small number of the remaining 83 institutions accounted for most of the outstanding investments. Specifically, 10 institutions accounted for $1.5 billion or about 73 percent of the $2.1 billion in outstanding investments. Treasury estimated a lifetime gain of $16.1 billion for CPP as of November 30, 2013.

Status of Capital Purchase Program Funds and Participants, as of January 31, 2014

GAO's analysis of financial data found that the institutions remaining in CPP were generally less financially healthy than those that have exited or that never participated. In particular, the remaining CPP institutions tended to be less profitable, hold riskier assets, and have lower capital levels and reserves. Most remaining participants also have missed scheduled dividend or interest payments, with 60 missing their November 2013 payment. Further, 47 of the remaining CPP institutions were on the Federal Deposit Insurance Corporation's problem bank list in December 2013—that is, they demonstrated financial, operational, or managerial weaknesses that threatened their continued financial viability. Institutions that continue to miss dividend payments or find themselves on the problem bank list may have difficulty fully repaying their CPP investments because federal and state bank regulators may not allow these institutions to make dividend payments or repurchase outstanding CPP shares in an effort to preserve their capital and promote safety and soundness.

Why GAO Did This Study

CPP was established as the primary means of restoring stability to the financial system under the Troubled Asset Relief Program (TARP). Under CPP, Treasury invested almost $205 billion in 707 eligible financial institutions between October 2008 and December 2009. CPP recipients have made dividend and interest payments to Treasury on the investments. TARP's authorizing legislation requires GAO to report every 60 days on TARP activities. This report examines (1) the status of CPP and (2) the financial condition of institutions remaining in the program.

To assess the program's status, GAO reviewed Treasury reports on the status of CPP. GAO also used financial and regulatory data to compare the financial condition of institutions remaining in CPP with those that had exited the program and those that did not participate. GAO also obtained information through a questionnaire from CPP participants as of November 20, 2013, and former CPP participants that raised capital in calendar year 2013. GAO received completed questionnaires from 72 of the 104 institutions.

GAO provided a draft of this report to Treasury for its review and comment. Treasury generally concurred with GAO's findings.

For more information, contact A. Nicole Clowers, 202-512-8678, clowersa@gao.gov.